Student Loan Forgiveness: New Bipartisan Bill Expands Programs by 10% in 2026

Policy Update: Congress Approves Bipartisan Bill to Expand Student Loan Forgiveness Programs by 10% Starting April 2026

In a landmark decision that promises to reshape the financial landscape for millions of Americans, Congress has officially approved a new bipartisan bill designed to significantly expand Student Loan Forgiveness programs. This pivotal legislation, which garnered support from both sides of the aisle, will increase the scope of existing forgiveness initiatives by an additional 10%, with the changes set to take effect in April 2026. This move marks a crucial step towards alleviating the burden of student debt and fostering greater economic mobility for a substantial portion of the population. The approval of this bill represents a collective recognition of the persistent challenges faced by borrowers and a commitment to providing tangible relief. The expanded Student Loan Forgiveness opportunities are expected to have far-reaching implications, impacting not only individual financial well-being but also contributing to broader economic stability. As we delve deeper into the specifics of this new policy, it becomes clear that its design aims to be both comprehensive and equitable, addressing various facets of student debt.

The journey to this legislative victory has been long and complex, characterized by extensive debates, negotiations, and a shared understanding of the urgent need for reform. Student loan debt has long been a pressing issue, affecting millions of households and often hindering major life milestones such as homeownership, starting a family, or pursuing entrepreneurial ventures. The existing forgiveness programs, while beneficial, have often been criticized for their complexity and limited reach. This new bipartisan bill seeks to address these shortcomings by simplifying access and broadening eligibility criteria, thereby making Student Loan Forgiveness a more accessible reality for a greater number of individuals. The 10% expansion is not merely a numerical increase; it signifies a strategic enhancement of the mechanisms through which borrowers can find relief. This expansion is projected to bring considerable financial respite to those who have been diligently managing their educational debts, offering a much-needed lifeline in an increasingly challenging economic climate. Understanding the nuances of this bill is paramount for anyone currently holding student debt or contemplating future educational financing. The introduction of these new provisions underscores a governmental commitment to supporting higher education and ensuring that the pursuit of knowledge does not come at an insurmountable financial cost.

Understanding the New Bipartisan Bill: Key Provisions and Enhancements for Student Loan Forgiveness

The recently approved bipartisan bill introduces several critical provisions that will redefine the landscape of Student Loan Forgiveness. At its core, the legislation aims to enhance and expand existing programs rather than creating entirely new ones from scratch. This approach ensures a smoother integration with current frameworks while significantly boosting their effectiveness. The primary highlight is the 10% increase in the total amount of debt that can be forgiven under various federal programs. This means that if a program previously offered forgiveness for a certain percentage of a loan balance, that percentage will now be increased by an additional 10 points. For instance, a program that offered 20% forgiveness might now offer 30%, or a program with a fixed dollar amount cap might see that cap increase by 10%. The specifics of how this 10% will be applied will vary depending on the particular forgiveness program in question, requiring borrowers to carefully review the updated guidelines once they are fully released.

Beyond the percentage increase, the bill also addresses several other areas critical to improving accessibility and fairness. One significant change includes a streamlining of the application process for Student Loan Forgiveness, reducing bureaucratic hurdles that have historically deterred many eligible borrowers. The legislation mandates the creation of a more user-friendly online portal and simplified documentation requirements, making it easier for individuals to understand their eligibility and submit necessary paperwork. Furthermore, there are provisions for increased outreach and education campaigns to ensure that potentially eligible borrowers are fully aware of the expanded opportunities available to them. This proactive approach aims to bridge the information gap that often prevents individuals from utilizing federal programs to their full extent. The bill also includes measures to improve the tracking and communication of borrowers’ progress towards forgiveness, offering greater transparency and reducing anxiety about the status of their applications. These combined efforts are designed to make the process of obtaining Student Loan Forgiveness more equitable and less daunting, empowering more individuals to take advantage of these vital relief options. The bipartisan nature of this bill is a testament to the widespread recognition of student debt as a national challenge requiring a unified response, and its provisions reflect a thoughtful, strategic approach to addressing this complex issue. The careful calibration of these enhancements suggests a long-term vision for sustainable student debt management, moving beyond short-term fixes towards systemic improvements.

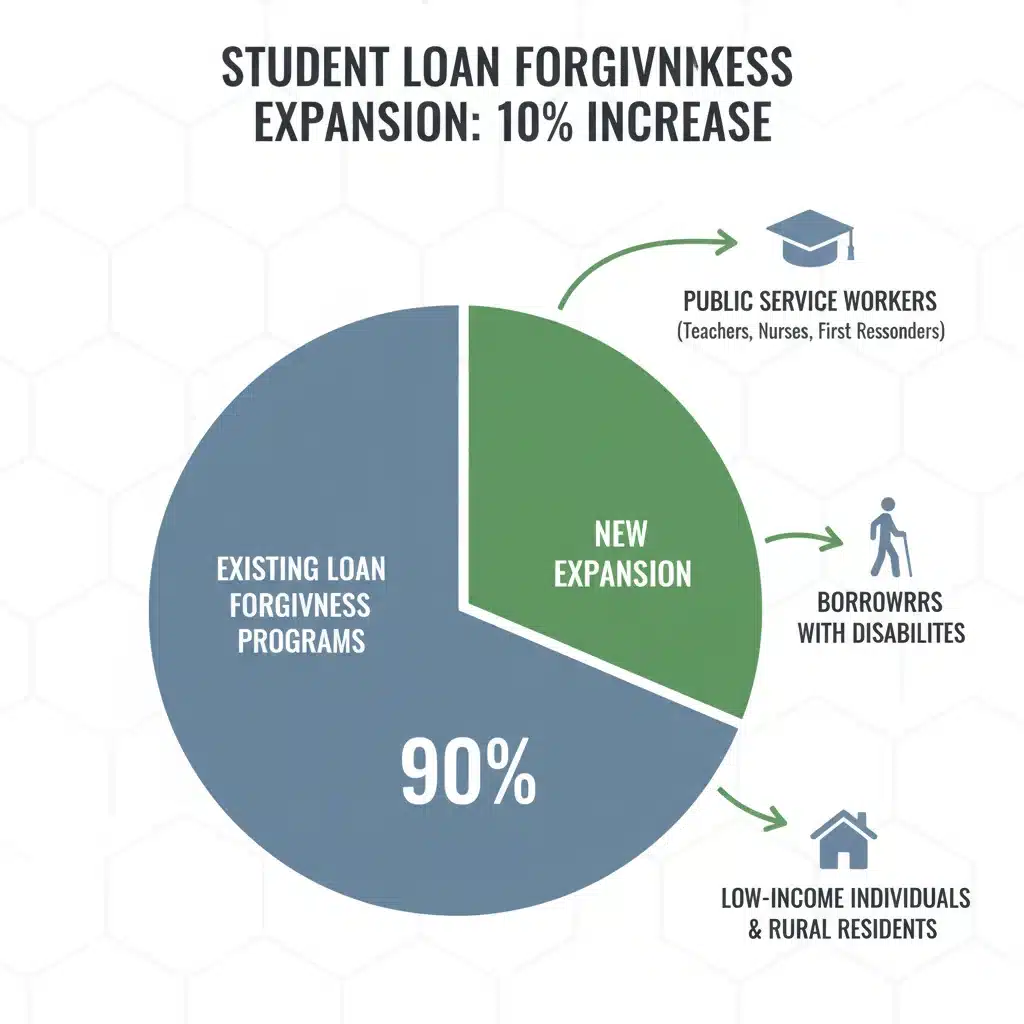

Who Benefits? Eligibility Criteria for Expanded Student Loan Forgiveness

One of the most crucial aspects of the new bipartisan bill is its impact on eligibility for Student Loan Forgiveness. While the 10% expansion is a broad enhancement, its benefits will be channeled through specific federal programs, meaning that certain borrower groups will be more directly affected than others. The legislation primarily targets existing federal student loan programs, including but not limited to, Public Service Loan Forgiveness (PSLF), income-driven repayment (IDR) plans leading to forgiveness, and specific teacher loan forgiveness programs. This means that borrowers with federal direct loans are most likely to see immediate benefits from these changes. Private student loans, generally, will not be covered by these federal expansions, underscoring the importance for borrowers to understand the distinction between federal and private debt.

For those already enrolled in or considering PSLF, the 10% expansion could translate into a shorter repayment period before forgiveness is granted, or a larger portion of their remaining balance being forgiven. The bill may also adjust the criteria for what constitutes “qualifying payments” or “eligible employment,” potentially broadening the pool of public service professionals who can benefit. Similarly, borrowers on IDR plans could see adjustments to their repayment schedules or an acceleration of their path to forgiveness, as the new provisions aim to reduce the overall time required to reach the forgiveness threshold. The exact mechanisms for these adjustments will be detailed in forthcoming guidance from the Department of Education. It is highly recommended that current and prospective borrowers stay informed about these updates to understand how their specific circumstances align with the new criteria for Student Loan Forgiveness.

Furthermore, the bill includes provisions that may offer specific relief to certain vulnerable populations. This could include borrowers who have been in repayment for an extended period, those with lower incomes, or individuals who have faced significant financial hardship. The bipartisan consensus on this issue highlights a shared commitment to ensuring that Student Loan Forgiveness is not just a theoretical possibility but a practical and attainable goal for those who need it most. The expanded eligibility aims to capture a wider demographic, ensuring that the relief is distributed more equitably across various income levels and career paths. As the implementation date of April 2026 approaches, the Department of Education will be releasing detailed guidelines and FAQs, which will be essential resources for all borrowers. These guidelines will clarify the specific changes to each program and provide clear instructions on how to take advantage of the expanded Student Loan Forgiveness opportunities. It is a critical time for borrowers to proactively engage with these updates and assess their own eligibility.

The Impact: What This Means for Borrowers and the Economy

The approval of this bipartisan bill and the subsequent 10% expansion of Student Loan Forgiveness programs are poised to generate significant impacts, both for individual borrowers and the broader national economy. For millions of Americans currently grappling with student debt, this legislation offers a tangible pathway to financial liberation. Reduced debt burdens can free up disposable income, allowing individuals to invest in their futures, stimulate local economies, and pursue long-delayed financial goals. This could translate into increased consumer spending, higher rates of homeownership, and greater participation in entrepreneurial activities, all of which contribute to a more robust economic environment. The psychological relief alone for many borrowers is immeasurable, reducing stress and improving overall well-being, which has its own positive ripple effects on productivity and quality of life.

Economically, the expansion of Student Loan Forgiveness is expected to have a stimulative effect. By injecting more capital into the hands of consumers, the policy can boost demand for goods and services, potentially leading to job creation and economic growth. While some critics might express concerns about the cost of such programs, proponents argue that the long-term economic benefits, including increased tax revenues from a more prosperous workforce and reduced reliance on social safety nets, will offset these initial expenditures. The bipartisan nature of the bill suggests a broad recognition of these potential economic upsides, moving past partisan divides to address a critical national issue. Furthermore, by addressing the student debt crisis, the government is investing in its human capital, ensuring that higher education remains a viable and beneficial pursuit for all citizens, not just those from affluent backgrounds.

The implications extend beyond just financial metrics. This policy shift can foster a more equitable society by providing opportunities for individuals from diverse socioeconomic backgrounds to achieve financial stability. It can also encourage more graduates to enter public service fields, such as teaching, nursing, and government work, knowing that their commitment to community will be supported by accessible Student Loan Forgiveness. This is particularly relevant for sectors that often face staffing shortages despite their critical importance to societal well-being. Ultimately, the bill aims to create a more sustainable and accessible higher education system, where the pursuit of knowledge is not unduly penalized by insurmountable debt. The implementation in April 2026 provides a reasonable timeline for both the government and borrowers to prepare for these changes, ensuring a smooth transition and maximizing the positive impact of this historic legislation. This comprehensive approach to student debt relief signifies a turning point in how educational financing is viewed and managed at a national level, promising a brighter financial future for many. The ripple effect of such a significant policy change will be felt across various sectors, demonstrating the interconnectedness of individual financial health and national economic prosperity. It’s a proactive measure designed to unlock potential and remove barriers that have long held back a segment of the population.

Preparing for April 2026: What Borrowers Need to Do Now for Student Loan Forgiveness

With the implementation of the expanded Student Loan Forgiveness programs slated for April 2026, borrowers have a crucial window of opportunity to prepare and ensure they are well-positioned to benefit from these changes. Proactive engagement with their loan servicers and the Department of Education will be key to maximizing the advantages offered by the new bipartisan bill. The first and most important step is to understand your current loan portfolio. Identify whether your loans are federal or private, as the expanded forgiveness primarily applies to federal student loans. If you have Federal Family Education Loan (FFEL) Program loans or Perkins Loans, you may need to consolidate them into a Direct Consolidation Loan to become eligible for certain federal forgiveness programs, including those that will be enhanced by the new bill. This consolidation process can take time, so it’s advisable to explore this option sooner rather than later.

Next, borrowers should review their current repayment plan. If you are not already on an income-driven repayment (IDR) plan, it may be beneficial to explore these options, as many of the forgiveness expansions are tied to these plans. The Department of Education website and your loan servicer can provide detailed information on the different IDR plans available and help you determine which one best suits your financial situation. Maintaining accurate records of all past payments, employment history (especially for PSLF candidates), and any correspondence with your loan servicer is also paramount. These records will be invaluable when applying for forgiveness or disputing any discrepancies that may arise. As the April 2026 date approaches, the Department of Education will release updated guidelines and application forms. It is critical to regularly check official government websites, such as StudentAid.gov, for the most current information and to ensure you are using the correct, updated forms. Subscribing to email updates from federal student aid resources can also help keep you informed.

Finally, consider seeking professional financial advice. A qualified financial advisor specializing in student loan debt can help you navigate the complexities of the new regulations, assess your eligibility for various programs, and develop a personalized strategy to take full advantage of the expanded Student Loan Forgiveness. They can also help you understand the potential tax implications of loan forgiveness, as some forgiven debt may be considered taxable income depending on your circumstances and the specific program. While the bipartisan bill offers significant relief, understanding its nuances and preparing adequately will be essential for all borrowers. By taking these proactive steps now, you can ensure that you are ready to seize the opportunities presented by this historic expansion of student loan forgiveness programs and move closer to financial freedom. The time between now and April 2026 is not merely a waiting period, but a strategic window for preparation and strategic planning to ensure you are optimally positioned to benefit from these significant policy changes. Don’t underestimate the power of being informed and prepared; it can make all the difference in navigating the path to debt relief.

The Broader Context: Why Student Loan Forgiveness Matters Now More Than Ever

The approval of the bipartisan bill to expand Student Loan Forgiveness by 10% in April 2026 arrives at a critical juncture for the United States economy and its workforce. The escalating cost of higher education has created a student debt crisis that has become a significant drag on economic growth and individual prosperity. For years, the burden of student loans has impacted major life decisions for millions, from delaying marriage and starting families to postponing homeownership and retirement savings. This new legislation acknowledges the systemic nature of this problem and offers a much-needed structural adjustment to help mitigate its adverse effects. It’s not just about individual relief; it’s about bolstering the foundational economic health of the nation by empowering its educated populace.

In an increasingly competitive global economy, a well-educated workforce is paramount. However, if the cost of obtaining that education becomes prohibitive, it can deter individuals from pursuing higher learning or force them into difficult financial situations post-graduation. The expansion of Student Loan Forgiveness aims to alleviate some of this pressure, making higher education a more sustainable investment. It can encourage more students to pursue degrees in high-demand fields, knowing that their future earning potential won’t be immediately swallowed by overwhelming debt. This can lead to a more skilled and innovative workforce, capable of driving technological advancements and economic competitiveness. The bipartisan nature of this bill underscores a rare consensus that addressing student debt is not merely a social justice issue but an economic imperative that transcends political ideologies.

Moreover, the timing of this expansion is particularly relevant in the wake of recent economic uncertainties. As the nation navigates fluctuating economic conditions, providing financial stability to a significant portion of the population can act as a buffer against broader economic downturns. When individuals are less burdened by debt, they are more resilient to economic shocks and more likely to contribute positively to the economy through spending and investment. This policy also represents a commitment to the long-term health of the education system itself. By making student loan repayment more manageable, it can foster greater trust in educational institutions and government programs designed to support students. This trust is vital for maintaining a robust and accessible higher education system that serves the needs of all Americans. The expanded Student Loan Forgiveness is therefore not just a financial transaction; it’s an investment in the future of the nation, its economy, and its people, ensuring that the pursuit of knowledge remains a pathway to opportunity rather than a source of lifelong financial strain. The policy reflects a forward-thinking approach, recognizing that the challenges of today require innovative and collaborative solutions for a prosperous tomorrow.

Conclusion: A New Era for Student Loan Forgiveness

The approval of the bipartisan bill to expand Student Loan Forgiveness programs by 10% starting April 2026 marks a significant milestone in the ongoing effort to tackle the nation’s student debt crisis. This legislative achievement, born from cross-party cooperation, reflects a collective understanding of the profound impact student debt has on millions of Americans and the broader economy. By enhancing existing federal programs and streamlining access, the bill promises to provide tangible financial relief, foster greater economic mobility, and strengthen the overall economic health of the country. The 10% expansion is more than just a number; it represents a strategic and impactful adjustment designed to make a real difference in the lives of borrowers.

As we look towards April 2026, the message to borrowers is clear: stay informed, prepare diligently, and actively engage with the resources available. Understanding the updated eligibility criteria, reviewing your loan status, and seeking professional guidance will be crucial steps in leveraging these expanded opportunities. This new era of Student Loan Forgiveness is not just about alleviating past burdens; it’s about paving the way for a more equitable and prosperous future where higher education remains a pathway to opportunity, not a source of insurmountable debt. The bipartisan bill stands as a testament to what can be achieved when policymakers unite to address critical national challenges, setting a precedent for future collaborative efforts. Its implementation will undoubtedly usher in a period of significant positive change for student loan borrowers across the United States, offering a renewed sense of hope and financial stability.