Navigating Student Loan Forgiveness: 2026 Graduates’ Guide to U.S. Policy Shifts

The journey through higher education is often accompanied by the significant financial burden of student loans. For the cohort of students poised to graduate in 2026, the landscape of student loan forgiveness is a dynamic and often confusing terrain, shaped by recent and ongoing U.S. policy shifts. Understanding these changes is not merely an academic exercise; it’s a critical step toward financial literacy and long-term economic well-being. This comprehensive guide aims to demystify the complexities of current and projected student loan policies, providing clarity and actionable insights for prospective 2026 graduates.

The past few years have witnessed unprecedented activity in federal student loan policy, from pandemic-related payment pauses to significant adjustments in existing forgiveness programs and the introduction of new initiatives. These shifts are not isolated events; they represent a concerted effort, albeit with varying degrees of success and political backing, to address the nation’s burgeoning student debt crisis. For those graduating in 2026, these policy changes will directly influence their repayment strategies, eligibility for relief, and overall financial outlook.

Our focus here is to equip you with the knowledge needed to navigate this evolving environment effectively. We will delve into the specifics of current forgiveness programs, analyze the impact of recent legislative and administrative actions, and provide forward-looking advice tailored for the 2026 graduating class. By the end of this article, you should have a clearer understanding of your potential options and how to best prepare for your post-graduation financial journey, keeping Student Loan Forgiveness 2026 firmly in view.

The Evolving Landscape of Student Loan Forgiveness for 2026 Graduates

The world of student loans is in a constant state of flux, and for those graduating in 2026, it’s particularly important to grasp the historical context and recent developments that will shape their repayment experience. The U.S. government has, over the years, introduced various programs designed to alleviate the burden of student debt, but these programs are frequently subject to review, modification, and sometimes, outright overhaul.

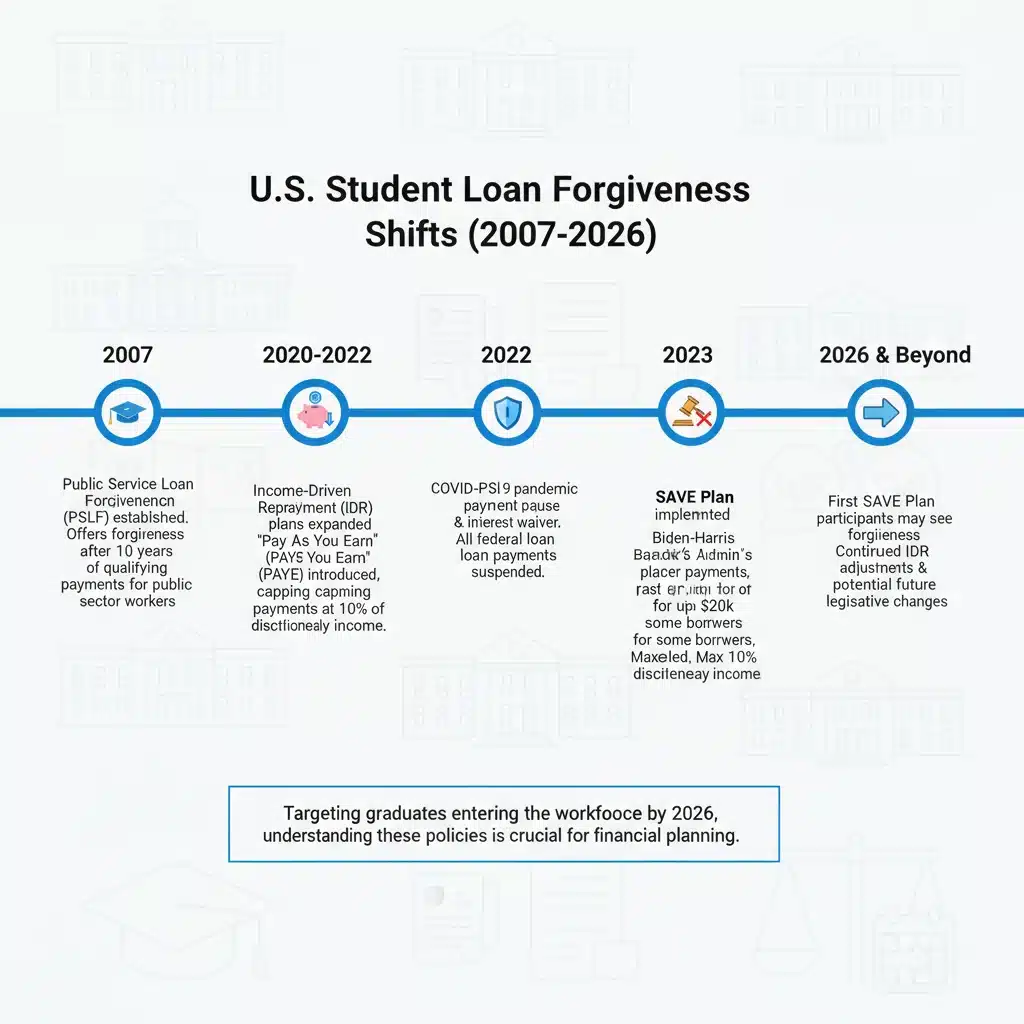

Historically, student loan forgiveness programs have primarily targeted specific professions or circumstances. The Public Service Loan Forgiveness (PSLF) program, for example, has been a cornerstone for individuals working in government or non-profit sectors. Income-Driven Repayment (IDR) plans have offered a safety net, allowing borrowers to make payments based on their income and family size, with the promise of forgiveness after a certain number of years. However, these programs have often been criticized for their complexity, administrative hurdles, and low approval rates.

The COVID-19 pandemic triggered an unprecedented pause on federal student loan payments and interest accumulation, providing a temporary reprieve for millions of borrowers. While this pause offered immediate relief, its eventual end brought renewed focus on long-term solutions. This period also saw significant discussions and attempts at broader, one-time loan forgiveness initiatives, though many of these faced legal challenges and political opposition, ultimately not coming to fruition in their originally proposed forms.

Post-pandemic, the Biden administration has pursued a strategy of targeted relief and administrative improvements to existing programs rather than sweeping, universal forgiveness. This has led to crucial adjustments within PSLF and IDR plans, aiming to simplify processes, correct past errors, and expand eligibility for forgiveness. These changes are particularly relevant for future graduates, as they lay the groundwork for how loan forgiveness will function in the years to come.

For the Class of 2026, these policy shifts mean that while the dream of widespread, automatic loan cancellation might remain elusive, significant opportunities for relief through existing, reformed programs are very much a reality. It’s no longer just about knowing the programs exist, but understanding their updated rules, revised eligibility criteria, and the proactive steps required to benefit from them. The key takeaway is that the federal government is actively working to refine its approach to student loan forgiveness, making it imperative for future borrowers to stay informed and engaged.

Key Policy Changes Affecting Future Loan Forgiveness

To fully understand your prospects for Student Loan Forgiveness 2026, it’s essential to examine the specific policy changes that have recently been enacted or are currently under consideration. These changes represent significant shifts from previous policies and will directly impact how forgiveness programs operate in the coming years.

Reforms to Income-Driven Repayment (IDR) Plans

One of the most impactful areas of reform has been within Income-Driven Repayment (IDR) plans. These plans are designed to make loan payments more manageable by capping them at a percentage of a borrower’s discretionary income, with any remaining balance forgiven after 20 or 25 years of qualifying payments. However, IDR plans have historically been plagued by issues, including administrative errors, miscounting of payments, and a lack of transparency.

Recent administrative actions have aimed to rectify these issues. The Department of Education has undertaken a one-time adjustment to IDR payment counts, which includes counting certain periods of deferment and forbearance that previously did not count towards forgiveness. This adjustment is particularly beneficial for long-term borrowers, potentially pushing many closer to forgiveness. For 2026 graduates, while they won’t directly benefit from past payment adjustments, the improved tracking and more accurate counting of future payments under IDR plans will be a significant advantage. The goal is to ensure that borrowers receive credit for every qualifying payment made, leading to more predictable and achievable forgiveness timelines.

Furthermore, discussions around new IDR plans, such as the SAVE (Saving on a Valuable Education) Plan, are critical. The SAVE Plan, for instance, proposes to significantly reduce monthly payments for many borrowers by lowering the percentage of discretionary income used to calculate payments and raising the amount of income protected from payment calculations. It also offers a provision for interest not to accrue if a borrower makes their full monthly payment, even if that payment is $0. These types of enhancements make IDR plans a much more viable and attractive path to forgiveness for future graduates struggling with their monthly obligations.

Public Service Loan Forgiveness (PSLF) Program Updates

The Public Service Loan Forgiveness (PSLF) program has also seen substantial reforms. PSLF offers forgiveness of the remaining balance on Direct Loans after 120 qualifying monthly payments (10 years) for borrowers working full-time for a qualifying government or non-profit organization. Historically, PSLF had a notoriously low approval rate due to complex rules, confusion over eligible employers, and issues with loan types.

The Limited PSLF Waiver, though temporary, provided an opportunity for many borrowers to count payments that previously didn’t qualify towards PSLF. While this waiver has largely concluded, its impact has led to permanent changes and a more flexible interpretation of PSLF rules. The Department of Education is now working to simplify the PSLF process, provide clearer guidance on eligible employment, and improve communication with borrowers. These improvements aim to make PSLF more accessible and less prone to administrative errors for future public servants.

For 2026 graduates considering careers in public service, these reforms are incredibly good news. The path to PSLF should be clearer, with fewer bureaucratic hurdles. It underscores the importance of ensuring you have the correct loan types (Direct Loans), are on a qualifying repayment plan (typically an IDR plan), and are diligently certifying your employment annually.

Beyond administrative changes, it’s crucial to acknowledge the potential for future legislative action. While broad loan forgiveness has faced political roadblocks, ongoing discussions in Congress could lead to new programs or further modifications to existing ones. The economic climate also plays a significant role; periods of economic downturn often spur calls for greater student debt relief.

For 2026 graduates, this means staying attuned to political developments and economic trends. While you can’t predict the future, being informed allows you to adapt your financial planning and quickly take advantage of any new opportunities that may arise. The landscape of Student Loan Forgiveness 2026 is not static, and proactive monitoring is key.

Eligibility and Requirements for 2026 Graduates

Understanding the eligibility criteria for student loan forgiveness programs is paramount for 2026 graduates. While the specific rules can be intricate, a clear grasp of the foundational requirements will empower you to make informed decisions about your loan repayment strategy and pursue potential relief. The phrase Student Loan Forgiveness 2026 implies a forward-looking approach to these qualifications.

Federal Student Loan Types: The Foundation of Forgiveness

First and foremost, nearly all federal student loan forgiveness programs apply exclusively to federal student loans. This is a critical distinction. Private student loans, issued by banks or other private lenders, are generally not eligible for federal forgiveness programs, including PSLF or IDR forgiveness. If you have a mix of federal and private loans, only the federal portion will be considered for these programs.

Within federal loans, Direct Loans are typically the most eligible. If you have older federal loans, such as Federal Family Education Loan (FFEL) Program loans or Perkins Loans, you may need to consolidate them into a Direct Consolidation Loan to become eligible for certain programs, particularly PSLF and some IDR benefits. This consolidation process is crucial and should be explored carefully, as it can sometimes affect interest rates or the timing of forgiveness.

Understanding Qualifying Employment for PSLF

For 2026 graduates aiming for Public Service Loan Forgiveness (PSLF), qualifying employment is the cornerstone. This means working full-time (generally 30 hours per week or more) for a:

- Government organization (federal, state, local, or tribal)

- 501(c)(3) non-profit organization

- Other non-profit organizations that provide specific public services

It’s important to note that the definition of "full-time" can sometimes be nuanced, especially if you work multiple part-time jobs. The Department of Education provides tools and guidance for certifying employment, and it’s highly recommended to use the PSLF Help Tool to confirm your employer’s eligibility and submit annual Employment Certification Forms. This proactive step helps track your progress and rectifies any potential issues early on, ensuring your path to Student Loan Forgiveness 2026 remains on track.

Navigating Income-Driven Repayment (IDR) Plans

Income-Driven Repayment (IDR) plans are often a prerequisite for PSLF and offer their own path to forgiveness after 20 or 25 years of payments. The key eligibility factors for IDR plans include:

- Federal Student Loans: As with PSLF, only federal loans are eligible.

- Income and Family Size: Your monthly payment is calculated based on a percentage of your discretionary income, which is your income above a certain poverty line threshold. Your family size also impacts this calculation, as a larger family generally means a lower discretionary income and thus a lower payment.

- Annual Certification: You must recertify your income and family size annually. Failing to do so can lead to your payments reverting to a standard plan or capitalized interest, which can significantly increase your loan balance.

For 2026 graduates, selecting the appropriate IDR plan (e.g., REPAYE, PAYE, IBR, or the new SAVE Plan) is a critical decision. Each plan has slightly different terms regarding payment percentages, interest subsidies, and forgiveness timelines. It’s advisable to use the Department of Education’s Loan Simulator tool to compare plans and determine which offers the best fit for your financial situation and long-term goals.

Other Forgiveness Programs and Special Circumstances

- Teacher Loan Forgiveness: For teachers who work for five consecutive complete school years in a low-income school or educational service agency.

- Perkins Loan Cancellation: For borrowers with Perkins Loans who work in certain public service professions.

- Total and Permanent Disability (TPD) Discharge: For borrowers who are unable to work due to a total and permanent disability.

- Borrower Defense to Repayment: For borrowers whose schools misled them or engaged in other misconduct.

- Closed School Discharge: For borrowers whose school closed while they were enrolled or shortly after they withdrew.

For 2026 graduates, it’s vital to assess if your chosen career path or personal circumstances align with any of these specialized programs. Each has its own distinct application process and eligibility criteria. Due diligence in researching these options can uncover significant relief opportunities.

Staying Compliant and Proactive

Regardless of the program you pursue, staying compliant and proactive is key. This includes:

- Keeping your contact information updated with your loan servicer.

- Making payments on time if you are not in an eligible deferment or forbearance.

- Retaining all financial and employment documentation.

- Regularly checking the Department of Education’s official websites for updates.

The rules for Student Loan Forgiveness 2026 are designed to provide relief, but the onus is on the borrower to understand and meet the requirements. Proactive engagement with your loan servicer and the Department of Education will significantly increase your chances of successfully navigating these programs.

Strategies for 2026 Graduates to Maximize Forgiveness

As a 2026 graduate, navigating the complexities of student loan forgiveness requires a strategic approach. Proactive planning and informed decision-making can significantly impact your eligibility and the amount of debt relief you ultimately receive. Here are key strategies to maximize your chances for Student Loan Forgiveness 2026.

1. Understand Your Loan Types and Consolidate if Necessary

The first and most critical step is to identify all your student loan types. Log into your Federal Student Aid account (studentaid.gov) to view your full loan portfolio. As mentioned, federal Direct Loans are generally the most eligible for forgiveness programs. If you have older FFEL or Perkins Loans, carefully consider consolidating them into a Direct Consolidation Loan. This step can make you eligible for PSLF and most IDR plans, but it’s essential to understand that consolidation creates a new loan with a new payment history, which could reset your payment count for forgiveness unless specific rules (like the IDR Account Adjustment) apply.

Consult with your loan servicer or a trusted financial advisor before consolidating to ensure it aligns with your long-term forgiveness goals. For 2026 graduates, making this decision early in your repayment journey is crucial.

2. Choose the Right Income-Driven Repayment (IDR) Plan

For most federal loan borrowers, an IDR plan is the pathway to forgiveness, either directly or as a prerequisite for PSLF. The Department of Education offers several IDR plans (REPAYE/SAVE, PAYE, IBR, ICR), each with different formulas for calculating monthly payments and different forgiveness timelines. The new SAVE plan, in particular, offers significant benefits for many borrowers, including lower monthly payments and a provision for unpaid interest not to capitalize.

Use the Loan Simulator tool on studentaid.gov to compare plans based on your income, family size, and loan balance. Select the plan that offers the lowest monthly payment and the quickest path to forgiveness for your situation. Remember to recertify your income and family size annually to ensure your payments remain accurate and you continue to qualify.

3. Diligently Track Public Service Employment for PSLF

If your career path involves public service, PSLF should be a primary consideration. Start tracking your qualifying employment from day one. Use the PSLF Help Tool on studentaid.gov to:

- Confirm your employer is eligible.

- Submit an Employment Certification Form (ECF) annually, or whenever you change employers.

Submitting ECFs regularly is vital. It allows the Department of Education to track your qualifying payments and identify any issues early, preventing costly surprises when you apply for forgiveness after 10 years. For 2026 graduates, consistent certification is key to maximizing PSLF opportunities.

4. Be Mindful of Deferment and Forbearance

While deferment and forbearance can provide temporary relief from payments, they generally do not count towards forgiveness under most programs. Recent IDR Account Adjustment changes have provided some flexibility for past periods, but for future payments, it’s safer to assume that payments made during deferment or forbearance will not count.

If you need to pause payments, explore options like a $0 payment under an IDR plan, which can still count towards forgiveness if your income is low enough. Only use deferment or forbearance as a last resort, and understand its implications for your forgiveness timeline. Proactive financial planning can help you avoid situations where these options become necessary.

5. Stay Informed About Policy Changes and Updates

The landscape of student loan policy is dynamic. What is true today regarding Student Loan Forgiveness 2026 might change tomorrow due to new legislation, administrative actions, or court rulings. Make it a habit to regularly check official sources such as:

- The U.S. Department of Education’s Federal Student Aid website (studentaid.gov).

- Your loan servicer’s website and communications.

- Reputable financial news outlets specializing in student debt.

Subscribing to newsletters or alerts from these sources can ensure you don’t miss critical updates that could impact your eligibility or open new avenues for relief.

6. Keep Meticulous Records

Maintain thorough records of all your student loan documents, including:

- Loan agreements and promissory notes.

- Correspondence with your loan servicer and the Department of Education.

- Records of all payments made.

- Employment certification forms (for PSLF).

- Income and family size documentation (for IDR).

These records will be invaluable if you ever need to dispute a payment count or prove your eligibility for a program. Digital copies, backed up securely, are highly recommended.

7. Consider Tax Implications of Forgiveness

While federal student loan forgiveness is generally tax-free through 2025 under the American Rescue Plan Act, it’s crucial for 2026 graduates to be aware that some forms of forgiveness might be considered taxable income at the state or federal level in the future. Forgiveness under PSLF is always tax-free federally. However, forgiveness under IDR plans after 20 or 25 years could potentially be taxed as income if the current federal tax exemption expires.

Consult with a tax professional as you approach your forgiveness date to understand any potential tax liabilities and plan accordingly. This foresight is part of a comprehensive strategy for Student Loan Forgiveness 2026.

The Role of Loan Servicers and How to Engage Them

Your loan servicer acts as the primary point of contact for your federal student loans. They handle billing, process payments, and provide information regarding repayment plans and forgiveness programs. Effectively engaging with your loan servicer is crucial for maximizing your chances of Student Loan Forgiveness 2026.

Understanding Your Loan Servicer’s Role

When you take out federal student loans, the U.S. Department of Education assigns your loan to a loan servicer. This servicer is responsible for:

- Sending you monthly statements and managing your payments.

- Providing information about repayment plans, including IDR plans.

- Helping you apply for deferment or forbearance.

- Collecting and processing documentation for programs like PSLF.

- Answering your questions about your loan balance, interest rates, and repayment options.

It’s important to remember that while servicers are there to assist, they are also contractors working for the Department of Education. Their primary role is to manage your loan, not necessarily to optimize your path to forgiveness. Therefore, while they can provide information, it’s ultimately your responsibility to understand the programs and ensure you meet the requirements.

Key Engagement Strategies with Your Loan Servicer

- Know Who Your Servicer Is: You can find your loan servicer by logging into your account on studentaid.gov. This is the first step to effective communication.

- Maintain Regular Communication: Don’t wait for a problem to arise. If you have questions about your repayment plan, eligibility for forgiveness, or need to update your contact information, reach out proactively. Keep a record of all communications, including dates, names of representatives, and summaries of conversations.

- Understand Your Repayment Plan Options: Discuss all available IDR plans with your servicer. Ask them to explain the differences, how your payments would be calculated under each, and the implications for forgiveness. Use the Loan Simulator on studentaid.gov as a tool to guide these conversations.

- Submit Documentation Promptly and Accurately: Whether it’s an Employment Certification Form for PSLF or annual income recertification for IDR, submit all required documentation well before deadlines. Double-check for accuracy and keep copies for your records.

- Escalate Issues When Necessary: If you believe your servicer has made an error, or if you’re not getting clear answers, don’t hesitate to escalate the issue. You can ask to speak with a supervisor. If the issue remains unresolved, you can file a complaint with the Federal Student Aid Ombudsman Group or the Consumer Financial Protection Bureau.

- Beware of Scams: Unfortunately, student loan scams are prevalent. Be wary of any company that charges a fee for services your servicer provides for free, or that promises immediate or guaranteed forgiveness. Always verify information with your official loan servicer or studentaid.gov.

For 2026 graduates, establishing a good working relationship with your loan servicer and understanding their role is a critical component of successfully managing your student debt and pursuing any available forgiveness. They are a resource, but you must be an active participant in the process.

Preparing for Your Post-Graduation Financial Journey

Graduating in 2026 marks the beginning of a new chapter, and with it comes the responsibility of managing your financial future, including student loans. Proactive preparation is key to navigating this journey successfully and maximizing your opportunities for Student Loan Forgiveness 2026.

1. Create a Comprehensive Budget

Before your grace period ends and loan payments begin, develop a detailed monthly budget. This budget should encompass all your income and expenses, including estimated student loan payments. Understanding your financial inflows and outflows will help you determine how much you can realistically afford to pay towards your loans and whether an IDR plan is necessary to make payments manageable. A realistic budget is the foundation of sound financial planning.

2. Understand Your Grace Period and First Payment Due Date

Most federal student loans have a grace period (typically six months) after you graduate, leave school, or drop below half-time enrollment before repayment begins. Use this time wisely. Do not wait until the last minute to understand your repayment options. Contact your loan servicer during your grace period to discuss plans and ensure you know your first payment due date. This proactive step prevents you from missing payments and potentially incurring penalties.

3. Build an Emergency Fund

Life is unpredictable, and having an emergency fund is crucial. Aim to save at least three to six months’ worth of essential living expenses. An emergency fund provides a buffer against unexpected job loss, medical emergencies, or other financial setbacks, preventing you from needing to rely on deferment or forbearance, which can extend your forgiveness timeline.

4. Explore Employer Benefits

Some employers offer student loan repayment assistance as part of their benefits package. Investigate whether your prospective or current employer provides such benefits. This could be a direct contribution to your loans or a matching program. Even if it’s not direct forgiveness, employer contributions can significantly reduce your principal balance and interest over time, indirectly helping you achieve your Student Loan Forgiveness 2026 goals.

5. Consider Refinancing Private Loans

If you have private student loans, consider whether refinancing them makes sense. Refinancing can potentially lower your interest rate or monthly payments, especially if your credit score has improved since you first took out the loans. However, remember that refinancing federal loans into private loans means losing access to federal benefits, including IDR plans and federal forgiveness opportunities. This decision should be made with careful consideration of its long-term implications.

6. Seek Professional Financial Advice

If you find the student loan landscape overwhelming, consider consulting a non-profit credit counselor or a certified financial planner. They can offer personalized advice, help you understand your options, and assist in creating a repayment strategy tailored to your specific situation and goals. Look for professionals who specialize in student debt and are transparent about their fees.

7. Focus on Long-Term Financial Health

Student loan repayment is just one aspect of your overall financial health. While pursuing forgiveness, also focus on other financial goals, such as saving for retirement, building credit, and planning for major life events. A holistic approach to your finances will ensure that student loan management fits into a broader strategy for economic stability and growth.

For 2026 graduates, the journey ahead is filled with opportunities and challenges. By understanding the policies, leveraging available resources, and adopting a proactive mindset, you can effectively manage your student loan debt and position yourself for a financially secure future. The path to Student Loan Forgiveness 2026 may require diligence and patience, but with the right strategies, it is an achievable goal.

Conclusion: Empowering 2026 Graduates for Student Loan Success

The landscape of U.S. student loan policy is undeniably complex, continuously evolving, and often a source of significant anxiety for graduates. However, for the class of 2026, understanding the recent shifts and available programs is not just an option but a necessity for informed financial decision-making. This guide has aimed to illuminate the path to Student Loan Forgiveness 2026, breaking down the intricacies of policy changes and outlining actionable strategies.

We’ve explored how crucial reforms to Income-Driven Repayment (IDR) plans and the Public Service Loan Forgiveness (PSLF) program are reshaping the possibilities for debt relief. The emphasis on improved payment counting, simplified processes, and potentially lower monthly payments under new IDR offerings like the SAVE Plan signifies a more accessible, albeit still nuanced, pathway to forgiveness. For public servants, the ongoing efforts to streamline PSLF provide renewed hope and clarity.

The key takeaway for 2026 graduates is the imperative of proactive engagement. Your student loan journey is not a passive one. It demands:

- Diligent Research: Continuously educate yourself on the specific terms of your loans and the nuances of each forgiveness program.

- Strategic Planning: Choose the right repayment plan (often an IDR plan) that aligns with your income, family size, and career goals.

- Meticulous Record-Keeping: Maintain comprehensive documentation of all communications, payments, and employment certifications.

- Consistent Communication: Regularly engage with your loan servicer and the Department of Education to ensure compliance and address any issues promptly.

- Adaptability: Stay informed about future legislative actions and economic conditions that could further alter the student loan landscape.

While the dream of broad, one-time loan cancellation might have faded, the reality of significant, targeted relief through reformed federal programs remains strong. For 2026 graduates, these programs represent tangible opportunities to alleviate the burden of student debt, allowing you to focus on building your careers, families, and futures without the overwhelming shadow of unmanageable loans.

By adopting the strategies outlined in this guide, you are not just reacting to policy changes; you are actively shaping your financial destiny. The path to Student Loan Forgiveness 2026 is within reach, requiring only your informed commitment and persistent effort. Empower yourself with knowledge, take control of your student loans, and embark on your post-graduation journey with confidence and financial clarity.