Student Loan Forgiveness 2026: Eligibility, Programs & Application Deadlines

The landscape of student loan debt in the United States is vast and often challenging to navigate. Millions of Americans grapple with the burden of student loans, making the prospect of Student Loan Forgiveness 2026 a beacon of hope for many. As we look towards 2026, understanding the various programs, eligibility requirements, and crucial application deadlines is paramount for anyone seeking relief from their educational debt. This comprehensive guide aims to demystify the complex world of student loan forgiveness, providing clear, actionable information to help you plan for your financial future.

The federal government, along with various state and private entities, offers a range of programs designed to alleviate student loan debt under specific circumstances. These programs are not one-size-fits-all, and their eligibility criteria can vary significantly. Whether you are a public servant, a teacher, a healthcare professional, or struggling with financial hardship, there might be a Student Loan Forgiveness 2026 option available for you. Staying informed about these opportunities and preparing for their application processes is the first step towards achieving financial freedom.

Understanding the Basics of Student Loan Forgiveness 2026

Before diving into specific programs, it’s essential to grasp the fundamental concepts behind student loan forgiveness. Essentially, student loan forgiveness means that you are no longer required to repay some or all of your federal student loans. It’s crucial to distinguish forgiveness from deferment or forbearance, which are temporary pauses in payments. Forgiveness, on the other hand, is a permanent cancellation of debt.

The availability and terms of Student Loan Forgiveness 2026 programs are subject to legislative changes and policy updates. While some programs are well-established, others may be introduced or modified based on economic conditions and political priorities. Therefore, continuous monitoring of official government sources, such as the U.S. Department of Education and Federal Student Aid (FSA) websites, is highly recommended.

It’s also important to note that most forgiveness programs target federal student loans. Private student loans generally do not qualify for federal forgiveness programs, although some private lenders may offer their own limited relief options. Therefore, identifying the type of loans you have is a critical first step in determining your eligibility for Student Loan Forgiveness 2026.

Key Terminology for Student Loan Forgiveness

- Federal Student Loans: Loans funded by the U.S. government, such as Direct Subsidized Loans, Direct Unsubsidized Loans, PLUS Loans, and Perkins Loans. These are typically eligible for forgiveness programs.

- Private Student Loans: Loans obtained from banks, credit unions, or other private lenders. These are generally not eligible for federal forgiveness programs.

- Default: Failure to make loan payments as scheduled. Defaulting on a loan can have severe consequences and may affect your eligibility for some forgiveness programs.

- Income-Driven Repayment (IDR) Plans: Repayment plans that base your monthly payment amount on your income and family size. Many forgiveness programs require participation in an IDR plan.

- Public Service: Employment with a government organization (federal, state, local, or tribal) or a not-for-profit organization that is tax-exempt under Section 501(c)(3) of the Internal Revenue Code.

Major Student Loan Forgiveness Programs for 2026

Several established federal programs offer significant opportunities for Student Loan Forgiveness 2026. Each program has specific criteria, and understanding these differences is key to identifying the best path for your situation.

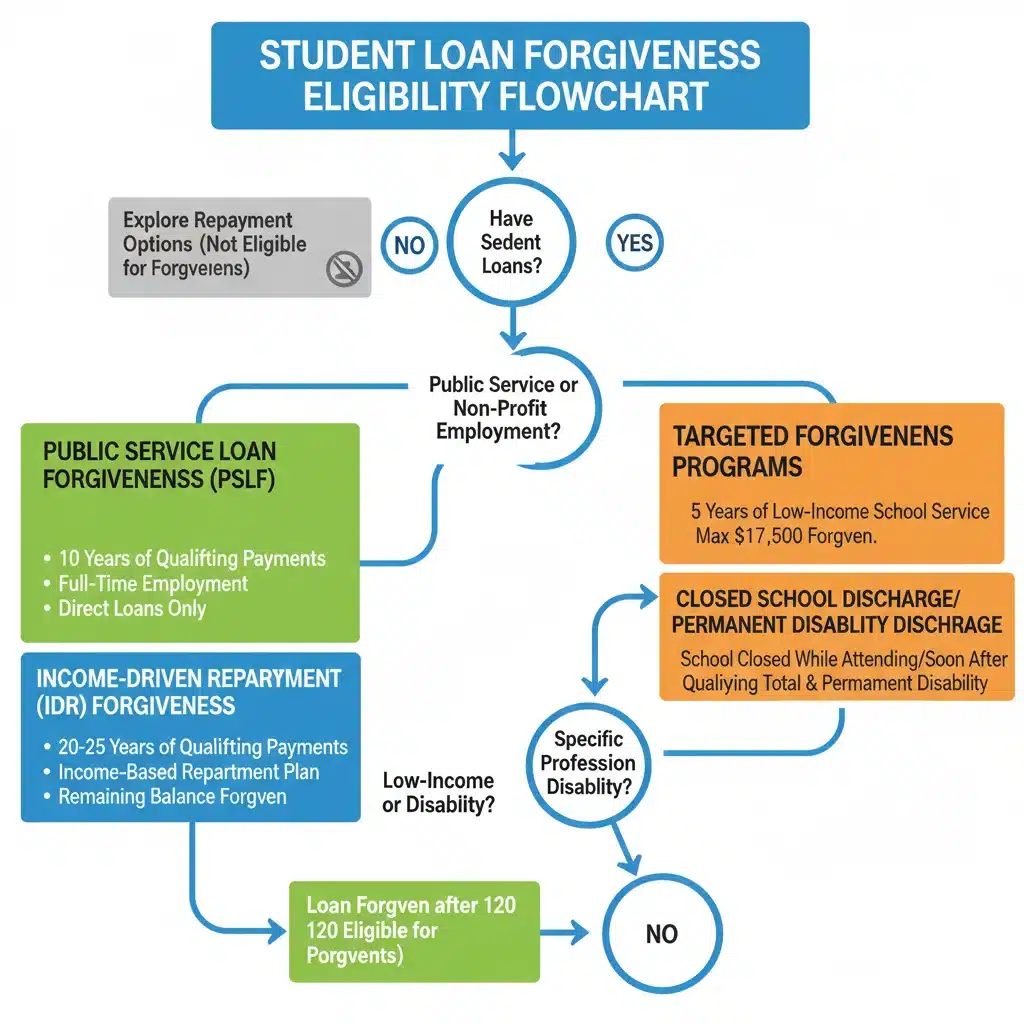

Public Service Loan Forgiveness (PSLF)

The PSLF program is designed to forgive the remaining balance on Direct Loans for borrowers who work full-time for qualifying public service employers. To be eligible for PSLF, you must:

- Be employed by a U.S. federal, state, local, or tribal government organization or a not-for-profit organization.

- Work full-time for that employer.

- Have Direct Loans (or consolidate other federal loans into a Direct Consolidation Loan).

- Make 120 qualifying monthly payments under a qualifying repayment plan (typically an IDR plan).

The 120 payments do not have to be consecutive, meaning you can change employers or take breaks from work, as long as you meet the full-time employment and payment requirements when you do make payments. The remaining balance on your Direct Loans is forgiven after you’ve made 120 qualifying payments.

It’s crucial to track your employment and payments carefully. The PSLF Help Tool is an invaluable resource provided by Federal Student Aid to help you determine if your employer qualifies and to submit your Employment Certification Form (ECF) annually or whenever you change employers. This proactive approach ensures that your payments are counted correctly towards the 120-payment requirement for Student Loan Forgiveness 2026 through PSLF.

Income-Driven Repayment (IDR) Plan Forgiveness

IDR plans are designed to make student loan payments more manageable by adjusting them based on your income and family size. There are several IDR plans, including:

- Revised Pay As You Earn (REPAYE) Plan

- Pay As You Earn (PAYE) Plan

- Income-Based Repayment (IBR) Plan

- Income-Contingent Repayment (ICR) Plan

Under these plans, any remaining loan balance is forgiven after 20 or 25 years of qualifying payments, depending on the specific plan and whether you have loans for graduate study. While the forgiveness period is longer than PSLF, it offers a path to relief for borrowers not in public service roles.

A significant aspect of IDR forgiveness to consider for Student Loan Forgiveness 2026 is the potential taxability of the forgiven amount. Unlike PSLF, IDR forgiveness can be considered taxable income by the IRS, unless Congress extends the current tax-free status for forgiven student loan debt. This is an important financial consideration to discuss with a tax professional.

Teacher Loan Forgiveness (TLF)

Teachers who serve for five complete and consecutive academic years in low-income schools or educational service agencies may be eligible for Teacher Loan Forgiveness. The amount of forgiveness depends on the subject taught:

- Up to $17,500 for highly qualified full-time math, science, or special education teachers.

- Up to $5,000 for highly qualified full-time elementary or secondary education teachers in other fields.

To qualify, you must have taken out your Direct Subsidized or Unsubsidized Loans, or your Federal Stafford Loans, after October 1, 1998. This program can be a great relief for educators dedicated to serving in high-need areas, contributing to their path for Student Loan Forgiveness 2026.

Loan Discharge for Total and Permanent Disability (TPD)

If you become totally and permanently disabled, you may be eligible for a discharge of your federal student loans. This discharge can be granted based on documentation from the Department of Veterans Affairs (VA), the Social Security Administration (SSA), or a physician’s certification. This program offers a critical safety net for those facing severe health challenges, allowing them to achieve Student Loan Forgiveness 2026.

There is typically a three-year monitoring period after discharge, during which you must meet certain income requirements and not take out new federal student loans. Failure to meet these conditions can result in the reinstatement of your discharged loans.

Closed School Discharge

If your school closed while you were enrolled, or shortly after you withdrew, you might be eligible for a 100% discharge of your federal student loans. This applies if you were unable to complete your program at that school or transfer your credits to another school. This discharge is designed to protect students who are left in a difficult position due to school closures.

Borrower Defense to Repayment Discharge

This program allows for the discharge of federal student loans if you can prove that your school engaged in misconduct or defrauded you. This can include misrepresentation of job placement rates, program accreditation, or other deceptive practices. Applications for borrower defense are reviewed on a case-by-case basis, and successful claims can lead to full or partial Student Loan Forgiveness 2026.

General Eligibility Criteria for Student Loan Forgiveness 2026

While each program has its specific requirements, some general eligibility criteria apply across many Student Loan Forgiveness 2026 options. Understanding these broad categories can help you quickly determine which programs might be relevant to your situation.

Loan Type Matters

As previously mentioned, most federal forgiveness programs apply exclusively to federal student loans. If you have Federal Family Education Loan (FFEL) Program loans or Perkins Loans, you might need to consolidate them into a Direct Consolidation Loan to become eligible for certain programs like PSLF or some IDR plans. Private loans are generally not eligible for federal forgiveness.

Employment Requirements

Many forgiveness programs are tied to specific types of employment. PSLF requires public service, TLF requires teaching in low-income schools, and some state-specific programs target healthcare professionals, lawyers, or other professionals in high-need areas. Verifying your employer’s eligibility and maintaining proper documentation of your employment history are vital steps.

Payment History and Repayment Plans

A consistent track record of on-time payments is often a prerequisite for forgiveness. For programs like PSLF and IDR, you must make a certain number of qualifying payments. These payments must typically be made under specific repayment plans, most commonly Income-Driven Repayment (IDR) plans. Enrolling in the correct plan and ensuring your payments are counted correctly is crucial for your Student Loan Forgiveness 2026 journey.

Financial Hardship or Disability

Some programs, like IDR plans, consider your income and family size to determine your payment amount, implicitly addressing financial hardship. Total and Permanent Disability (TPD) discharge directly addresses situations where a borrower’s disability prevents them from working and earning a living. These programs provide essential relief for those facing significant financial or health challenges.

Application Processes and Deadlines for Student Loan Forgiveness 2026

Navigating the application process for Student Loan Forgiveness 2026 can be complex, but with careful planning and attention to detail, it is entirely manageable. Each program has its own set of forms and procedures, and missing a deadline can significantly delay or even disqualify you from relief.

Steps to Apply for Forgiveness

- Identify Your Loan Type: Log in to your Federal Student Aid account (StudentAid.gov) to view all your federal student loans. This will help you determine which programs you might qualify for.

- Research Programs: Based on your loan type, employment, and personal circumstances, research the specific forgiveness programs that align with your situation.

- Consolidate Loans (if necessary): If you have FFEL or Perkins Loans and want to pursue PSLF or certain IDR plans, you may need to consolidate them into a Direct Consolidation Loan. Be aware that consolidation can sometimes reset your payment count for forgiveness programs, so consult with your loan servicer first.

- Enroll in an IDR Plan: If your chosen forgiveness program requires payments under an IDR plan, ensure you are enrolled and recertify your income and family size annually.

- Track Your Progress: For PSLF, use the PSLF Help Tool to submit your Employment Certification Form (ECF) regularly. For IDR forgiveness, keep records of all your payments and annual recertifications.

- Submit Your Application: Once you meet all eligibility requirements (e.g., 120 qualifying payments for PSLF), submit the official application for forgiveness.

Important Deadlines to Watch For

While there isn’t a single universal deadline for all Student Loan Forgiveness 2026 programs, several key dates and recurring deadlines are critical to keep in mind:

- Annual IDR Recertification: If you’re on an Income-Driven Repayment (IDR) plan, you must recertify your income and family size annually. Missing this deadline can lead to higher monthly payments or even removal from the IDR plan, potentially jeopardizing your progress toward IDR forgiveness.

- PSLF Employment Certification: Although not strictly a deadline, submitting the PSLF Employment Certification Form (ECF) annually or whenever you change employers is highly recommended. This ensures your qualifying payments are accurately tracked and any issues can be addressed proactively.

- Temporary Waivers and Expedited Processes: In recent years, the Department of Education has introduced temporary waivers (like the PSLF Waiver and the IDR Account Adjustment) that have allowed more borrowers to qualify for forgiveness by counting previously ineligible payments. While these waivers have had specific end dates, it’s essential to stay informed about any new or extended relief initiatives that might arise in 2026.

- Program-Specific Deadlines: For programs like Teacher Loan Forgiveness or specific state-based programs, there may be application windows or deadlines tied to the completion of service requirements. Always check the official program guidelines for precise dates.

- Changes in Legislation: Policy changes can impact existing programs or introduce new ones. Stay updated on legislative developments that could create new opportunities for Student Loan Forgiveness 2026 or alter existing eligibility requirements and deadlines.

State and Profession-Specific Loan Forgiveness Programs

Beyond federal initiatives, many states and specific professions offer their own loan forgiveness or repayment assistance programs. These are often designed to address workforce shortages in critical areas or to incentivize professionals to work in underserved communities. Exploring these options can significantly broaden your opportunities for Student Loan Forgiveness 2026.

Healthcare Professionals

Many states and federal agencies offer programs for doctors, nurses, dentists, and other healthcare providers who agree to work in health professional shortage areas (HPSAs). Examples include:

- National Health Service Corps (NHSC) Loan Repayment Program: Offers significant loan repayment for primary care medical, dental, and mental/behavioral health providers who serve in HPSAs.

- Nurse Corps Loan Repayment Program: Provides loan repayment to registered nurses and advanced practice registered nurses working in eligible facilities in underserved areas or serving as nurse faculty.

Law Professionals

Law school graduates who pursue careers in public interest law, government service, or legal aid organizations may find state or university-sponsored loan repayment assistance programs (LRAPs). These programs aim to alleviate the financial burden that might otherwise deter graduates from taking lower-paying public service legal roles.

Other Professions

Teachers (beyond federal TLF), veterinarians, engineers, and other professionals may also find state or local programs offering loan forgiveness or repayment assistance. These programs often have specific service requirements, such as working in a particular geographic area or for a certain type of employer for a set number of years. Always check with your state’s education department or professional licensing boards for relevant programs.

Tax Implications of Student Loan Forgiveness 2026

One critical aspect of Student Loan Forgiveness 2026 that often gets overlooked until it’s too late is the tax implications. While receiving forgiveness can be a huge relief, it’s essential to understand how the IRS views this cancelled debt.

Historically, forgiven debt from Income-Driven Repayment (IDR) plans has been considered taxable income. This means that if you have $50,000 forgiven, that amount could be added to your taxable income for the year, potentially resulting in a significant tax bill. However, under the American Rescue Plan Act of 2021, most student loan forgiveness was made tax-free at the federal level until December 31, 2025. This means any forgiveness received before this date will not be subject to federal income tax.

As we approach 2026, it is uncertain whether this tax-free status will be extended. Therefore, for any IDR forgiveness received in 2026 and beyond, you should assume it will be taxable unless new legislation is passed. It is crucial to consult with a tax professional to understand your specific situation and plan for any potential tax liability associated with Student Loan Forgiveness 2026.

It’s important to note that Public Service Loan Forgiveness (PSLF) is generally tax-free at the federal level, and this has historically been the case. This is a significant advantage of the PSLF program. State tax laws can vary, so even if federal forgiveness is tax-free, check your state’s regulations.

Avoiding Student Loan Forgiveness Scams

Unfortunately, the promise of Student Loan Forgiveness 2026 also attracts scammers. Be extremely wary of companies or individuals who promise guaranteed forgiveness, demand upfront fees, or ask for your FSA ID or other sensitive personal information. Legitimate forgiveness programs are always free to apply for, and you will work directly with your loan servicer or the Department of Education.

Signs of a scam include:

- Promises of immediate or guaranteed forgiveness.

- Requests for payment to access forgiveness programs.

- Pressure to act quickly or claims of secret programs.

- Requests for your FSA ID, which should never be shared.

Always verify information with official sources like Federal Student Aid (StudentAid.gov) or your direct loan servicer. If something sounds too good to be true, it probably is.

The Future Outlook for Student Loan Forgiveness Beyond 2026

The landscape of student loan relief is constantly evolving. While this guide focuses on Student Loan Forgiveness 2026, it’s important to recognize that future policy changes could introduce new programs, modify existing ones, or impact eligibility and deadlines. The political climate, economic conditions, and ongoing debates about higher education financing all play a role in shaping these policies.

Advocacy groups continue to push for broader student debt relief, and various legislative proposals are always under consideration. Staying engaged with reliable news sources and official government announcements will help you remain informed about any potential changes that could affect your student loan situation in the years to come.

For now, the best strategy is to focus on the established programs, understand their requirements, and proactively manage your loans. By doing so, you position yourself to take advantage of any Student Loan Forgiveness 2026 opportunities that align with your circumstances.

Conclusion: Your Path to Student Loan Forgiveness 2026

Navigating the world of student loan forgiveness requires diligence, patience, and a clear understanding of the available options. The prospect of Student Loan Forgiveness 2026 offers a tangible pathway to financial relief for many borrowers, but it’s not a passive process. You must actively research, apply, and monitor your eligibility and progress.

Start by identifying your loan types, exploring federal programs like PSLF, IDR forgiveness, and TLF, and investigating state or profession-specific options. Pay close attention to eligibility criteria, understand the application processes, and mark crucial deadlines on your calendar. Be vigilant against scams and always rely on official sources for information.

By taking these steps, you can empower yourself to make informed decisions about your student loan debt and potentially secure significant financial relief in 2026 and beyond. The journey to Student Loan Forgiveness 2026 may seem daunting, but with the right information and proactive engagement, it is an achievable goal for many.