2026 COLA Increase: What a 3.2% Adjustment Means for Your Benefits

The 2026 COLA Increase: How a Projected 3.2% Adjustment Shapes Your Future Payments

As we look towards the horizon of 2026, millions of Americans relying on Social Security and Supplemental Security Income (SSI) benefits are keenly awaiting news regarding the annual Cost-of-Living Adjustment (COLA). The projected 2026 COLA increase of 3.2% is more than just a number; it represents a critical adjustment designed to help beneficiaries keep pace with inflation and maintain their purchasing power. For retirees, individuals with disabilities, and their families, understanding the intricacies of this adjustment is paramount for effective financial planning and peace of mind.

The COLA is a vital mechanism that prevents the erosion of benefits due to rising costs of living. Without these annual adjustments, the fixed income of many beneficiaries would gradually lose value, making it increasingly difficult to afford necessities. This comprehensive guide will delve deep into the projected 3.2% 2026 COLA increase, exploring its calculation, historical context, and the profound impact it will have on both retirement and disability payments. We will also discuss strategies for beneficiaries to navigate these changes and maximize their financial well-being.

Understanding the COLA Basics: What is it and Why Does it Matter?

Before we dissect the projected 2026 COLA increase, it’s essential to grasp the fundamental concept of the Cost-of-Living Adjustment. COLA is an annual increase in Social Security and SSI benefits to offset the effects of inflation. It ensures that the purchasing power of these benefits does not erode over time. The Social Security Administration (SSA) determines the COLA based on changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

The CPI-W measures the average change over time in the prices paid by urban wage earners and clerical workers for a market basket of consumer goods and services. This basket includes food, housing, apparel, transportation, medical care, recreation, and education. By tracking these price changes, the SSA can determine how much more expensive everyday life has become, and thus, how much benefits need to increase to maintain a consistent standard of living for beneficiaries.

The significance of COLA cannot be overstated. For many seniors and individuals with disabilities, Social Security benefits represent a substantial, if not sole, source of income. Without regular adjustments, rising costs for groceries, utilities, healthcare, and housing would quickly diminish the real value of their benefits, leading to financial hardship. The 2026 COLA increase, therefore, serves as a crucial safeguard against the relentless march of inflation.

How the 3.2% 2026 COLA Increase is Calculated

The calculation of the COLA is a precise process, dictated by federal law. The Social Security Act specifies that the COLA is based on the percentage increase in the CPI-W from the third quarter of the previous year to the third quarter of the current year. Specifically, the average CPI-W for July, August, and September is compared to the average CPI-W for the same three months of the last year in which a COLA was effective.

For the 2026 COLA increase, the SSA will compare the average CPI-W for the third quarter of 2025 to the average CPI-W for the third quarter of 2024. If there is an increase, the percentage difference, rounded to the nearest tenth of a percent, becomes the COLA for the following year. If there is no increase, or if prices decrease, there is no COLA for that year, meaning benefits remain unchanged.

The 3.2% projection for the 2026 COLA increase is based on current economic forecasts and inflation trends. These projections are made by various organizations, including the Social Security Administration’s actuaries, the Congressional Budget Office, and private economic forecasting firms. While these are projections and not final figures, they provide beneficiaries and policymakers with an early indication of what to expect. The official COLA announcement typically occurs in October of the preceding year (e.g., October 2025 for the 2026 COLA).

It’s important to note that the CPI-W doesn’t always perfectly reflect the spending patterns of all Social Security beneficiaries, particularly seniors who may have higher healthcare costs. This has led to ongoing discussions about alternative inflation measures, such as the CPI-E (Consumer Price Index for the Elderly), which could potentially result in higher COLA adjustments in some years. However, for the foreseeable future, the CPI-W remains the congressionally mandated index for COLA calculations.

Impact on Retirement Payments: Navigating Your Financial Future with the 2026 COLA Increase

For millions of retirees, the 2026 COLA increase will directly translate into higher monthly Social Security checks. A 3.2% adjustment, while not as dramatic as some recent COLAs, is still a significant boost that can help mitigate the ongoing effects of inflation on fixed incomes. Let’s consider an example: if a retiree currently receives $1,800 per month in Social Security benefits, a 3.2% COLA would increase their payment by $57.60, bringing their new monthly benefit to $1,857.60. While this might seem like a modest increase, over a year, it amounts to an additional $691.20, which can make a tangible difference in covering rising expenses.

The impact of the 2026 COLA increase extends beyond just the raw dollar amount. It affects the purchasing power of retirees, allowing them to maintain their standard of living amidst rising costs for essentials like groceries, utilities, and prescription medications. Without this adjustment, the real value of their benefits would diminish, forcing difficult choices about spending or potentially drawing down savings faster.

However, it’s also crucial for retirees to understand that while their Social Security payments increase, other financial aspects might also be affected. For instance, the increase could push some beneficiaries into a higher income bracket, potentially leading to a larger portion of their Social Security benefits being subject to federal income tax. Additionally, for those receiving other government benefits that are means-tested, the COLA increase could, in rare cases, affect their eligibility or the amount of those benefits. Therefore, comprehensive financial planning is essential to fully understand the net impact of the 2026 COLA increase.

Disability Payments and the 2026 COLA Increase: Support for Those in Need

Just like retirement benefits, Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) payments are also subject to the annual COLA. This means that individuals receiving disability benefits can expect their monthly payments to increase by the projected 3.2% 2026 COLA increase. This adjustment is particularly critical for disability beneficiaries, many of whom have limited income earning capacity due to their medical conditions.

For an individual receiving the average SSDI benefit, which was approximately $1,537 per month in 2023, a 3.2% COLA would add about $49.18 to their monthly check, resulting in a new payment of $1,586.18. For SSI beneficiaries, whose maximum federal benefit is lower, the percentage increase still provides much-needed relief from inflation. These increases help cover the rising costs of living, including specialized medical care, transportation to appointments, and other disability-related expenses.

However, similar to retirement benefits, disability beneficiaries also need to be aware of potential secondary effects. For SSI recipients, whose eligibility is strictly means-tested, an increase in Social Security benefits (if they receive both) could potentially impact their SSI payment amount, though the COLA is designed to prevent a reduction in overall purchasing power. It is always advisable for disability beneficiaries to review their financial situation and consult with benefit specialists if they have concerns about how the 2026 COLA increase might affect their overall benefit package or other assistance programs they rely on.

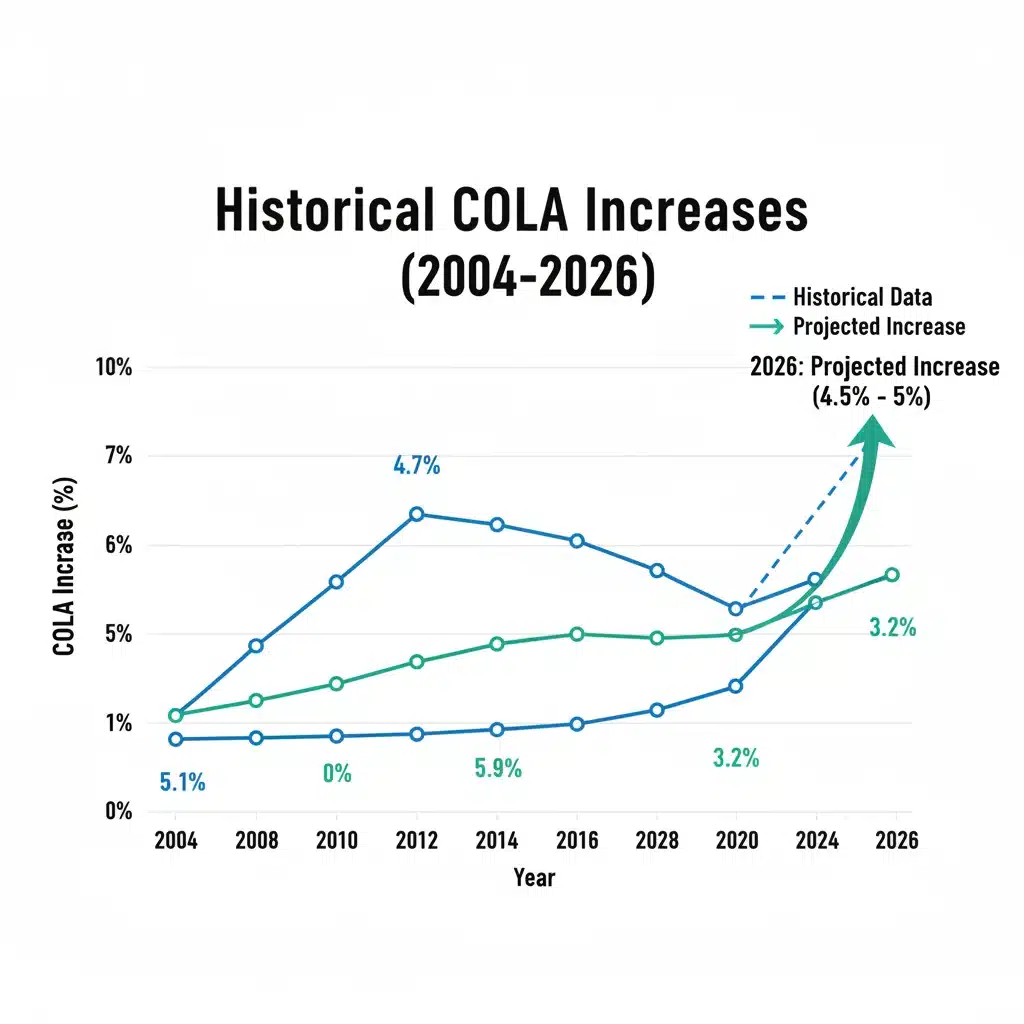

Historical COLA Trends and the Significance of the 2026 COLA Increase

To fully appreciate the projected 3.2% 2026 COLA increase, it’s helpful to look at it within the context of historical trends. Over the past few decades, COLA percentages have varied significantly, reflecting different economic environments and inflation rates. For instance, in periods of high inflation, such as the early 1980s, COLAs were in the double digits. Conversely, during periods of low inflation or even deflation, COLAs have been very low or even zero, as seen in 2009, 2010, and 2015.

More recently, the COLA for 2023 was a substantial 8.7%, driven by a surge in inflation in 2022. The 2024 COLA was 3.2%, and the 2025 COLA is projected to be around 2.6%. The anticipated 3.2% for the 2026 COLA increase suggests a continued, albeit more moderate, inflationary environment. This level of increase is generally considered healthy, reflecting economic growth without the runaway inflation that can severely impact fixed-income earners.

Understanding these trends helps beneficiaries contextualize the upcoming adjustment. A moderate COLA like the projected 3.2% for 2026 indicates that while inflation is still a factor, it is not spiraling out of control. This provides a degree of predictability for financial planning, allowing individuals to anticipate a reasonable boost to their benefits without the volatility of extreme economic fluctuations.

Examining historical data also underscores the critical role COLA plays in the long-term solvency of Social Security. While COLAs are essential for beneficiaries, they also represent a significant expenditure for the Social Security trust funds. The balancing act between providing adequate benefits and ensuring the long-term financial health of the program is a constant challenge for policymakers.

Financial Planning Strategies in Light of the 2026 COLA Increase

For all Social Security beneficiaries, the projected 3.2% 2026 COLA increase presents an opportunity to review and adjust their financial plans. Here are several strategies to consider:

- Re-evaluate Your Budget: With an increase in monthly income, even a modest one, it’s a good time to revisit your household budget. Identify areas where you can allocate the extra funds, whether it’s towards rising costs, savings, or discretionary spending.

- Address Rising Healthcare Costs: Healthcare expenses are a significant concern for many seniors and individuals with disabilities. The 2026 COLA increase can help offset some of the increases in Medicare premiums, deductibles, and out-of-pocket costs. Ensure you understand how your Medicare Part B premium might be affected, as it is often deducted directly from Social Security benefits.

- Consider Tax Implications: As mentioned earlier, higher Social Security income can sometimes lead to a larger portion of benefits being taxable. Consult with a tax advisor to understand your specific situation and plan accordingly, especially if your overall income is close to the thresholds for taxing Social Security benefits.

- Boost Your Savings: If your essential expenses are covered, consider directing a portion of the 2026 COLA increase into a savings account or an emergency fund. Having a financial cushion is always prudent, especially in retirement or when managing a disability.

- Review Other Benefits: If you receive other government assistance programs, check if the COLA increase could impact your eligibility or benefit amounts. While most programs are designed to coordinate with Social Security, it’s always best to verify.

- Invest in Yourself: Perhaps the extra funds can be used for something that improves your quality of life, such as a new hobby, educational course, or home improvement that enhances accessibility.

Proactive financial planning ensures that the 2026 COLA increase serves its intended purpose: to enhance your financial security and maintain your standard of living.

The Future of COLA and Social Security: Beyond the 2026 COLA Increase

While the focus is currently on the projected 3.2% 2026 COLA increase, it’s important to consider the broader context of COLA and the long-term solvency of the Social Security program. Debates about the COLA calculation method, the overall financial health of Social Security, and potential reforms are ongoing in Washington. Some proposals suggest using a different inflation index, like the CPI-E, which is believed to better reflect the spending patterns of seniors. Others focus on broader reforms to address the long-term funding challenges faced by the program.

The Social Security Administration’s annual Trustees’ Report provides detailed projections on the program’s financial status. These reports often highlight the need for adjustments to ensure that Social Security can continue to pay full benefits for future generations. While the 2026 COLA increase is a certainty (assuming inflation exists), the mechanism and funding for future COLAs and benefits are subject to legislative decisions.

Beneficiaries and concerned citizens are encouraged to stay informed about these policy discussions. Understanding the potential changes to COLA calculations or the Social Security program itself can help individuals plan for their long-term financial security. Advocacy groups often provide valuable resources and opportunities to engage in these important conversations.

How to Stay Informed About the 2026 COLA Increase and Beyond

Staying updated on Social Security news, especially regarding the 2026 COLA increase and subsequent adjustments, is crucial. Here are reliable sources of information:

- Social Security Administration (SSA) Website: The official source for all COLA announcements and detailed information about benefits. Visit ssa.gov.

- SSA My Social Security Account: Create an online account to view your earnings record, estimated benefits, and receive updates directly from the SSA.

- Reputable Financial News Outlets: Major financial news sources often provide analysis and updates on COLA projections and economic factors influencing them.

- Congressional Budget Office (CBO): The CBO provides independent analyses and projections, including those related to Social Security and economic indicators.

- AARP: This organization often publishes articles and guides specifically for seniors regarding Social Security and related benefits.

By regularly checking these sources, you can ensure you have the most accurate and up-to-date information regarding the 2026 COLA increase and any other relevant changes that may impact your benefits.

Conclusion: Preparing for the 2026 COLA Increase

The projected 3.2% 2026 COLA increase is a significant development for millions of Social Security and SSI beneficiaries. It represents the government’s commitment to protecting the purchasing power of those who rely on these vital programs. While the official announcement is still some time away, understanding the calculation, historical context, and potential impacts of this adjustment now allows for proactive financial planning.

Whether you are a retiree planning your budget, an individual with a disability managing healthcare costs, or someone simply interested in the future of Social Security, the 2026 COLA increase will play a role in your financial landscape. By staying informed, re-evaluating your financial strategies, and utilizing available resources, you can effectively navigate these changes and ensure your benefits continue to provide the support you need to maintain your quality of life.

Remember that Social Security is a dynamic program, constantly adapting to economic realities. The 2026 COLA increase is just one piece of this larger puzzle, but an incredibly important one that directly touches the lives of millions of Americans. Prepare now, stay informed, and secure your financial future.