Navigating 3.5% Inflation: Safeguarding Your 2026 Retirement Savings

In the intricate landscape of personal finance, few factors exert as profound an influence on our long-term goals as inflation. As we cast our gaze towards 2026, the prospect of a sustained 3.5% inflation rate looms large, presenting a significant challenge to those meticulously planning for their retirement. Understanding the nuances of how this seemingly modest percentage can erode your purchasing power and diminish the real value of your savings is not merely an academic exercise; it is a critical imperative for anyone aiming to secure a comfortable and financially independent future. This comprehensive guide delves deep into the mechanisms of inflation, its specific implications for your retirement savings by 2026, and, most importantly, equips you with actionable strategies to mitigate its adverse effects and even turn potential threats into opportunities.

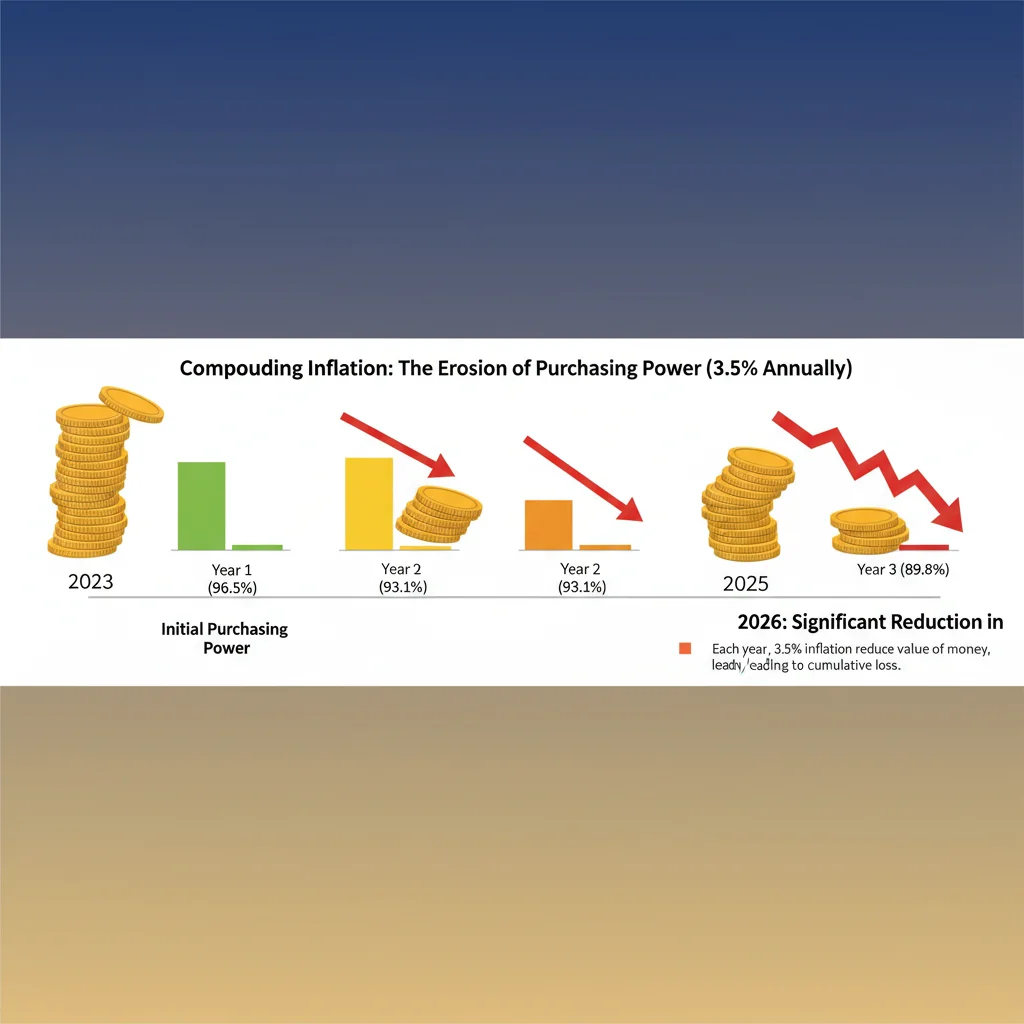

The journey to retirement is often envisioned as a steady accumulation of wealth, where each dollar saved today contributes to a more secure tomorrow. However, inflation acts as an invisible tax, stealthily chipping away at the value of those accumulated dollars. A 3.5% inflation rate, while not historically unprecedented, is substantial enough to warrant serious attention, especially for those with a finite timeline to retirement, such as 2026. This rate means that an item costing $100 today will cost approximately $103.50 next year, and this compounding effect can significantly alter your financial landscape over several years. For retirement planning, where horizons often span decades, even a moderate inflation rate can have a dramatic impact on the real value of your future income and expenses.

Our goal here is to demystify the complex interplay between inflation and your retirement portfolio. We will explore how different asset classes react to inflationary pressures, identify common pitfalls to avoid, and present a robust framework for adjusting your financial strategies. From re-evaluating your investment mix to considering inflation-indexed securities and understanding the role of real assets, this article provides a holistic perspective designed to empower you with the knowledge and tools necessary to protect and grow your wealth in an inflationary environment. By the end of this read, you will have a clearer understanding of the challenges ahead and a well-defined roadmap to navigate them successfully, ensuring that your inflation retirement 2026 plans remain firmly on track.

Understanding the Basics of Inflation and Its Impact on Retirement

Before we delve into specific strategies, it’s crucial to solidify our understanding of inflation itself. Inflation refers to the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. When economists speak of a 3.5% inflation rate, they are suggesting that, on average, the cost of living will increase by that percentage annually. While this might seem manageable in the short term, its long-term implications for retirement savings are profound. Imagine you have $100,000 saved today. With a consistent 3.5% inflation rate, in just five years, the purchasing power of that $100,000 will be significantly less. In real terms, it would only be equivalent to roughly $84,000 in today’s money. This erosion of value directly impacts your ability to cover future expenses, from daily living costs to healthcare and leisure activities during retirement.

For those targeting retirement in 2026, this means that every dollar saved between now and then, and every dollar already saved, will be worth less than its face value upon withdrawal. The cost of goods and services you expect to purchase in retirement will be higher than current prices, necessitating a larger nest egg than you might initially calculate using today’s figures. This phenomenon is particularly critical for fixed-income retirees, whose income streams may not keep pace with rising costs, further exacerbating the challenge. Therefore, simply saving money is not enough; your savings must grow at a rate that outpaces inflation to maintain or increase their real value.

The primary concern for your inflation retirement 2026 strategy is the preservation of purchasing power. If your investments yield a nominal return of, say, 5% annually, but inflation runs at 3.5%, your real return is only 1.5%. While still positive, this significantly slows the growth of your wealth in terms of what it can actually buy. If your investments yield less than the inflation rate, you are effectively losing money in real terms, even if your account balance appears to be increasing. This fundamental concept underscores the importance of actively managing your portfolio with inflation in mind, rather than passively observing its effects.

The 2026 Horizon: Specific Challenges and Considerations

The year 2026 is a relatively short time horizon for retirement planning, making the impact of a 3.5% inflation rate even more immediate and pronounced. Unlike those with decades until retirement who can ride out short-term fluctuations, individuals nearing retirement in 2026 have less time to recover from inflationary erosion or to implement aggressive long-term growth strategies. This necessitates a more focused and perhaps conservative yet effective approach to safeguard their accumulated wealth.

One of the main challenges is that many traditional retirement portfolios, especially those designed for individuals nearing retirement, tend to be more heavily weighted towards fixed-income assets like bonds. While bonds offer stability and lower volatility, they are often highly susceptible to inflation. If bond yields do not adequately compensate for inflation, their real returns can turn negative, meaning your principal’s purchasing power diminishes over time. This makes a careful re-evaluation of your asset allocation paramount.

Furthermore, lifestyle expectations for retirement in 2026 need to be critically assessed against this inflationary backdrop. What you project as your monthly expenses today will likely be insufficient to cover the same standard of living in 2026. This applies to everything from housing costs, utilities, groceries, transportation, to healthcare – a particularly significant expenditure for retirees. Failing to account for these increased costs can lead to a shortfall in your retirement income, forcing unwanted compromises in your golden years. Therefore, updating your retirement budget with an inflation-adjusted lens is a crucial step for your inflation retirement 2026 planning.

Strategies to Mitigate Inflation’s Impact on Your 2026 Retirement Savings

Navigating a 3.5% inflation rate requires proactive and strategic financial planning. Here are several key strategies to consider as you approach your 2026 retirement:

1. Re-evaluate Your Asset Allocation and Diversify

Diversification is always a cornerstone of sound investment, but it becomes even more critical during inflationary periods. While bonds might traditionally be considered safer, their vulnerability to inflation means you might need to adjust your exposure. Consider a more balanced approach that includes assets historically known to perform well during inflation:

- Equities (Stocks): Companies that can pass on increased costs to consumers through higher prices often perform well during inflationary times. Look for companies with strong pricing power, robust balance sheets, and consistent earnings growth. A diversified portfolio of blue-chip stocks, dividend-paying stocks, or even index funds can offer a hedge against inflation.

- Real Estate: Real assets, including real estate, tend to hold their value and often appreciate with inflation. Rental income can also increase, providing a growing stream of income. Consider direct investment in properties, Real Estate Investment Trusts (REITs), or real estate-focused mutual funds.

- Commodities: Gold, silver, oil, and other raw materials often serve as inflation hedges. As the cost of goods rises, so too do the prices of the materials used to produce them. While volatile, a small allocation to commodities can provide diversification.

- Treasury Inflation-Protected Securities (TIPS): These are government bonds whose principal value adjusts with the Consumer Price Index (CPI). When inflation rises, the principal value of TIPS increases, and so do the interest payments. This makes them a direct and effective hedge against inflation.

The key is not to put all your eggs in one basket. A thoughtful blend of these asset classes can help ensure that at least a portion of your portfolio keeps pace with or outpaces inflation, thus protecting your purchasing power for your inflation retirement 2026.

2. Consider Inflation-Indexed Annuities

While annuities can be complex, some types offer inflation protection. An inflation-indexed annuity provides payments that increase over time, typically tied to a measure of inflation like the CPI. This ensures that your fixed income stream in retirement doesn’t lose its purchasing power. While they might offer lower initial payouts compared to traditional annuities, the long-term benefit of increasing income can be invaluable in a persistent inflationary environment. Consult with a financial advisor to determine if such a product aligns with your overall retirement strategy and risk tolerance.

3. Optimize Your Income Streams for Retirement

Beyond investments, consider how your retirement income streams will be affected. If you plan to rely heavily on Social Security, remember that benefits are adjusted annually for inflation through Cost-of-Living Adjustments (COLAs). However, these adjustments may not always fully keep pace with your personal inflation rate, especially for specific expenses like healthcare. For private pensions, check if they offer COLAs. If not, you may need to supplement this income with other inflation-protected assets.

For those still working, consider delaying retirement slightly if feasible. An extra year or two of work can allow for additional savings, increased Social Security benefits by delaying claims, and more time for investments to compound before you begin withdrawals. This extra buffer can be crucial in mitigating the effects of inflation retirement 2026.

4. Focus on Reducing Debt Before Retirement

High-interest debt can become an even greater burden during inflationary periods. As the cost of living rises, your discretionary income may shrink, making it harder to service debt. Prioritizing the repayment of high-interest consumer debt, credit card balances, and even mortgages before retirement can free up significant cash flow in your golden years. This reduces your reliance on a potentially shrinking retirement income to cover essential expenses, providing greater financial flexibility and peace of mind.

5. Revisit Your Retirement Budget with Inflation in Mind

It’s imperative to update your retirement budget to reflect projected costs in 2026 and beyond. Don’t simply use today’s prices. Factor in the 3.5% inflation rate for major expenditure categories. For example, if you anticipate spending $5,000 per month today, by 2026 (assuming a 3.5% annual inflation rate for three years), that same lifestyle could cost approximately $5,540 per month. This revised budget will give you a more realistic target for your required savings and income, allowing you to adjust your investment and withdrawal strategies accordingly.

6. Healthcare Costs: A Special Consideration

Healthcare inflation often outpaces general inflation. As you approach retirement, particularly by 2026, healthcare costs will likely be one of your largest and most unpredictable expenses. Factor in potential increases in insurance premiums, deductibles, co-pays, and prescription drug costs. Consider options like Health Savings Accounts (HSAs) if you are eligible, as they offer a triple tax advantage (tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses) and can be an excellent way to save for future medical costs. Planning for these escalating expenses is a critical component of safeguarding your inflation retirement 2026.

Advanced Strategies and Professional Guidance

For those with more complex financial situations or a greater desire for tailored guidance, engaging with a financial advisor specializing in retirement planning is highly recommended. A qualified professional can help you:

- Develop a Personalized Inflation-Adjusted Plan: An advisor can create a bespoke financial plan that accounts for your specific risk tolerance, income needs, and asset base, explicitly incorporating inflation projections for 2026 and beyond.

- Optimize Tax Efficiency: Inflation can interact with taxes in complex ways. An advisor can help you structure your withdrawals and investments to minimize your tax burden, thereby maximizing your real returns.

- Explore Alternative Investments: Beyond traditional stocks and bonds, there are other asset classes that can offer inflation protection, such as private equity, infrastructure funds, or even certain structured products. An advisor can assess if these are suitable for your portfolio.

- Regular Portfolio Reviews: The economic landscape is dynamic. Regular reviews with an advisor ensure your strategy remains resilient and adaptable to changing inflationary pressures and market conditions.

The value of professional guidance cannot be overstated, especially when facing critical financial milestones like retirement during periods of elevated inflation. They can provide an objective perspective and help you avoid emotional decisions that could jeopardize your long-term financial security for your inflation retirement 2026.

The Psychological Aspect: Staying Calm and Focused

Inflationary periods can evoke anxiety and uncertainty, potentially leading to impulsive financial decisions. It’s crucial to maintain a calm and rational approach. Avoid panic selling during market downturns that might be exacerbated by inflation fears. Stick to your well-researched financial plan and make adjustments based on sound principles, not fleeting headlines. Remember that financial markets are inherently volatile, and long-term success often comes from patience and disciplined adherence to a strategic course.

Educating yourself, as you are doing by reading this article, is one of the best defenses against financial anxiety. The more you understand about how inflation works and how it affects your money, the more confident you will be in your ability to navigate these challenges. Focus on what you can control: your savings rate, your investment choices, your debt levels, and your spending habits. These personal financial disciplines are powerful tools in combating the effects of inflation on your retirement.

Conclusion: Proactive Planning for a Secure 2026 Retirement

The prospect of a 3.5% inflation rate by 2026, while a significant factor, does not have to derail your retirement plans. Instead, it serves as a powerful call to action for proactive and intelligent financial planning. By understanding the mechanics of inflation, carefully re-evaluating your asset allocation, optimizing your income streams, and diligently managing your expenses and debt, you can effectively safeguard the real value of your retirement savings.

The journey to a secure retirement is dynamic, requiring continuous attention and adaptation. For those eyeing 2026 as their retirement year, the time to act is now. Implement the strategies discussed, seek professional advice where needed, and remain vigilant in monitoring economic indicators. With a well-thought-out plan and disciplined execution, you can not only mitigate the challenges posed by inflation but also ensure that your golden years are characterized by financial freedom and peace of mind. Your proactive efforts today in managing the impact of inflation retirement 2026 will undoubtedly pave the way for a more comfortable and fulfilling future.