Digital Banking Adoption Soars: 15% Increase by 2026

The financial landscape is undergoing a profound transformation, driven by rapid technological advancements and evolving consumer expectations. A recent, groundbreaking report has illuminated this shift, projecting a significant 15% increase in digital banking adoption across U.S. adults by March 2026. This isn’t just a fleeting trend; it’s a fundamental reorientation of how individuals interact with their financial institutions, marking a pivotal moment in the history of banking. The implications of this surge are far-reaching, affecting everything from product development and customer service to regulatory frameworks and market competition.

For years, the promise of digital banking has been whispered among fintech innovators and forward-thinking financial institutions. Now, that promise is translating into tangible growth, with millions of Americans embracing the convenience, efficiency, and accessibility that digital platforms offer. This article delves deep into the findings of this report, exploring the underlying factors contributing to this remarkable growth in digital banking adoption, the innovative technologies making it possible, the challenges that still need to be addressed, and what the future holds for a financial world increasingly defined by digital interactions.

Understanding the Surge in Digital Banking Adoption

The 15% projected increase in digital banking adoption is not an isolated phenomenon; it’s the culmination of several converging forces. The COVID-19 pandemic, for instance, acted as a significant catalyst, forcing many consumers and businesses to rely on digital channels for their financial needs when physical branches were inaccessible. This period of forced adoption introduced a wider demographic to the benefits of online and mobile banking, dispelling previous hesitations and fostering a new level of comfort with digital financial services.

Beyond the pandemic, a generational shift is also at play. Younger generations, particularly Millennials and Gen Z, have grown up in a digitally native world. They expect seamless, intuitive, and always-on access to services, and banking is no exception. For them, digital banking isn’t a novelty; it’s the default. As these demographics gain more economic power, their preferences are increasingly shaping the market.

Moreover, traditional banks have significantly invested in their digital infrastructure, recognizing the imperative to evolve. They’ve enhanced their mobile apps, streamlined online platforms, and integrated new features that rival those offered by challenger banks and fintech startups. This competitive pressure has spurred innovation across the entire banking sector, ultimately benefiting the consumer.

The report highlights several key metrics contributing to this growth, including an increase in mobile banking app usage for daily transactions, a rise in digital-only account openings, and a greater reliance on online platforms for managing investments and loans. This comprehensive shift indicates that consumers are not just using digital channels for basic tasks but are increasingly entrusting their entire financial lives to these platforms. The widespread availability of high-speed internet, coupled with the ubiquity of smartphones, has created an environment where digital banking adoption can thrive, offering unparalleled convenience and accessibility to financial services from virtually anywhere at any time.

Technological Innovations Fueling the Growth

The impressive growth in digital banking adoption would not be possible without continuous technological innovation. Financial technology (fintech) companies and traditional banks are constantly pushing the boundaries of what’s possible, introducing features that enhance user experience, security, and functionality.

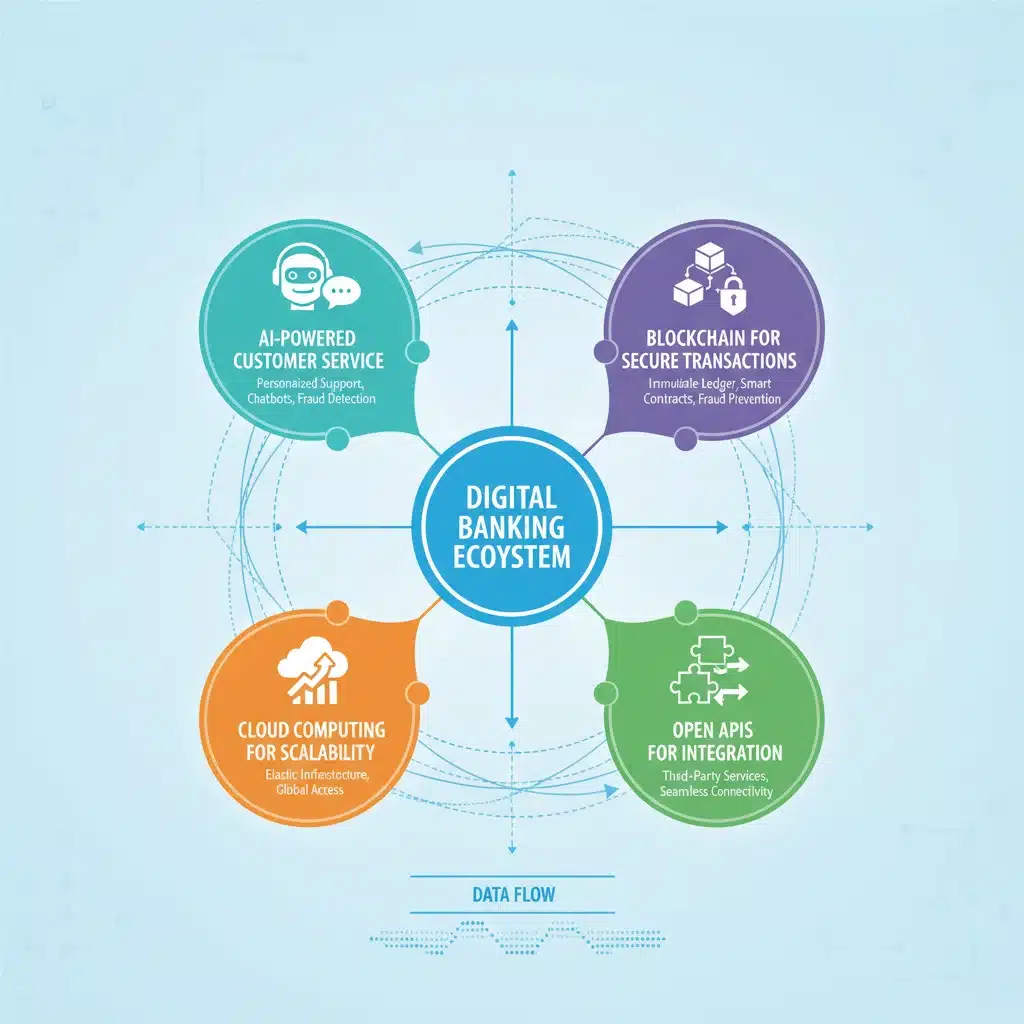

One of the most significant advancements is the integration of Artificial Intelligence (AI) and Machine Learning (ML). These technologies power intelligent chatbots for customer support, provide personalized financial advice, detect fraudulent activities with greater accuracy, and offer predictive analytics to help users manage their money more effectively. Imagine a banking app that not only shows you your spending habits but also predicts your future cash flow based on your historical data and upcoming bills – this is the power of AI at work.

Blockchain technology, while still in its nascent stages for many consumer applications, is also playing a role, particularly in enhancing the security and transparency of transactions. Cryptocurrencies, built on blockchain, have introduced a new paradigm of digital assets, and while not directly tied to traditional digital banking, their underlying technology is influencing how financial data is secured and transferred. Secure authentication methods, such as multi-factor authentication (MFA) and biometric logins (fingerprint, facial recognition), have become standard, assuaging consumer fears about the security of their digital accounts and further bolstering confidence in digital banking adoption.

Cloud computing is another foundational technology enabling the scalability and flexibility required for modern digital banking platforms. Banks can now process vast amounts of data, deploy new features rapidly, and adapt to changing market demands without the heavy upfront infrastructure costs of traditional systems. This agility allows them to remain competitive and responsive to consumer needs, directly contributing to the increasing rates of digital banking adoption.

Furthermore, the rise of Open Banking APIs (Application Programming Interfaces) is fostering an ecosystem of interconnected financial services. This allows third-party developers to create innovative applications that integrate with banking data (with user consent), offering services like budgeting tools, investment trackers, and personalized financial dashboards that pull information from multiple accounts. This interoperability creates a richer, more comprehensive financial experience for users, making digital banking more attractive and versatile than ever before.

The Impact on Traditional Banking Institutions

The rapid increase in digital banking adoption presents both opportunities and challenges for traditional banking institutions. On one hand, it allows them to reach a wider customer base, reduce operational costs associated with physical branches, and offer a more personalized and efficient service. By leveraging digital channels, banks can automate routine tasks, freeing up human resources to focus on more complex customer needs and relationship building.

However, the shift also demands significant investment in technology and a cultural transformation within these organizations. Banks must compete not only with other traditional banks but also with agile fintech startups that are often unburdened by legacy systems and regulations. This competition is driving an urgency to innovate, to not just offer digital services but to excel at them.

Many traditional banks are responding by adopting a ‘digital-first’ strategy, prioritizing the development of their online and mobile platforms. They are also forming partnerships with fintech companies to integrate specialized services and leverage cutting-edge technologies that they might not have the in-house expertise to develop. This collaborative approach helps accelerate their digital transformation and ensures they remain relevant in an increasingly digital world. The success of these initiatives is crucial for maintaining market share and attracting new customers amidst the rising tide of digital banking adoption.

Another significant impact is on the branch network. While physical branches are unlikely to disappear entirely, their role is evolving. They are becoming more focused on complex transactions, financial advice, and community engagement rather than simple deposits and withdrawals, which are now predominantly handled digitally. This shift requires a re-evaluation of branch design, staffing, and operational models to complement the digital offerings rather than compete with them. The future of banking is undoubtedly hybrid, with digital and physical channels working in concert to provide a holistic customer experience.

Benefits for U.S. Adults and the Economy

The widespread digital banking adoption brings a multitude of benefits to U.S. adults and the broader economy. For individuals, the most immediate benefit is unparalleled convenience. Banking from home, work, or on the go eliminates the need for physical visits to branches, saving time and effort. This is particularly beneficial for those in rural areas or individuals with mobility challenges, effectively democratizing access to financial services.

Enhanced financial management tools are another key advantage. Digital platforms often provide real-time insights into spending, budgeting tools, investment tracking, and alerts for unusual activity, empowering users to take greater control of their finances. This can lead to better financial literacy and more informed decision-making, ultimately improving individual financial well-being.

From an economic perspective, increased digital banking adoption can lead to greater efficiency in financial markets. Faster transaction processing, reduced paperwork, and lower operational costs for banks can translate into more competitive rates and innovative products for consumers. It also fosters a more inclusive financial system, bringing traditionally underserved populations into the banking fold through accessible digital channels, which can stimulate economic growth and reduce financial inequality.

Furthermore, the data generated by digital banking interactions, when anonymized and aggregated, can provide valuable insights for economic analysis and policy-making. This data can help identify emerging trends, assess financial health, and inform strategies to support economic stability and growth. The overall impact is a more dynamic, responsive, and resilient financial sector that better serves the needs of a modern society.

Challenges and Considerations for Future Growth

Despite the optimistic projections for digital banking adoption, several challenges and considerations need to be addressed to ensure sustainable and equitable growth. Cybersecurity remains a paramount concern. As more financial transactions move online, the risk of cyberattacks, data breaches, and fraud increases. Banks and fintech companies must continuously invest in robust security measures, educate users on best practices, and adapt to evolving threats to maintain consumer trust. A single major security incident could significantly erode confidence and hinder adoption rates.

Digital literacy is another critical factor. While younger generations are digitally native, a significant portion of the adult population, particularly older demographics, may lack the necessary skills or comfort level to fully embrace digital banking. Financial institutions have a responsibility to provide clear, accessible educational resources and intuitive user interfaces to bridge this digital divide. Ensuring that digital banking is accessible to everyone, regardless of their technological proficiency, is crucial for truly widespread adoption.

Regulatory frameworks also need to evolve to keep pace with technological advancements. Regulators face the delicate task of fostering innovation while protecting consumers and maintaining financial stability. Issues such as data privacy, consumer protection in an AI-driven environment, and the regulation of new financial products and services require careful consideration and adaptation of existing laws. A clear and consistent regulatory environment is essential for providing certainty to financial institutions and encouraging further investment in digital solutions.

Finally, the human element cannot be overlooked. While digital channels offer immense convenience, there will always be a segment of the population that prefers human interaction for complex financial decisions or simply for reassurance. Striking the right balance between digital efficiency and personalized human service will be key to long-term success. The focus should be on integrating digital tools to augment human capabilities, rather than entirely replacing them, ensuring that the increasing digital banking adoption enhances the overall customer experience without alienating any segment of the population.

The Future Outlook for Digital Banking

Looking ahead, the trajectory of digital banking adoption appears set for continued growth and innovation. The 15% increase projected by March 2026 is likely just a waypoint on a much longer journey towards a fully digitized financial ecosystem. Several trends are expected to define this future.

Hyper-personalization, driven by advanced AI and data analytics, will become even more sophisticated. Banks will be able to offer highly tailored products, services, and advice based on individual financial behaviors, life events, and goals, making banking feel less transactional and more like a personalized financial partnership. This level of customization will further enhance the appeal and utility of digital banking platforms, driving deeper engagement and satisfaction among users.

Embedded finance, where financial services are seamlessly integrated into non-financial platforms (e.g., buying insurance when purchasing a car online, or getting a loan offer at the point of sale), will become more prevalent. This makes financial services even more accessible and convenient, reducing friction and expanding the reach of digital banking beyond traditional channels. The blurring lines between financial and non-financial services will create new opportunities for innovation and collaboration, further accelerating digital banking adoption.

The metaverse and Web3 technologies, while still in early development, also hold potential for future digital banking experiences. Imagine conducting financial transactions, receiving advice, or even attending virtual branch meetings in an immersive 3D environment. While these concepts are futuristic, the underlying principles of decentralization, digital ownership, and immersive experiences could eventually shape how we interact with our money in the digital realm. Banks are already exploring these frontiers, understanding that staying ahead of technological curves is essential for continued relevance.

Cross-border payments will become faster, cheaper, and more transparent, thanks to innovations in blockchain and real-time payment systems. This will significantly benefit individuals and businesses engaged in international trade and remittances, further solidifying the global reach and impact of digital banking. The focus will increasingly be on creating a truly global, interconnected financial network that operates with the speed and efficiency of the internet itself.

Finally, sustainability and ethical considerations will play a larger role. Consumers are increasingly demanding that their financial institutions align with their values. Digital banking platforms can offer tools to track the environmental impact of spending, invest in socially responsible funds, and support ethical banking practices. This integration of values with financial services will not only attract a new generation of conscious consumers but also ensure that the growth in digital banking adoption is aligned with broader societal goals.

Conclusion

The report projecting a 15% increase in digital banking adoption across U.S. adults by March 2026 is a clear indicator of a profound and irreversible shift in the financial services industry. This growth is a testament to the power of technological innovation, the evolving demands of consumers, and the strategic investments made by financial institutions. Digital banking offers unparalleled convenience, enhanced financial management tools, and greater accessibility, benefiting both individuals and the broader economy.

While challenges related to cybersecurity, digital literacy, and regulatory adaptation remain, the industry is actively working to address these issues. The future of banking is undoubtedly digital, characterized by hyper-personalization, embedded finance, and potentially new immersive experiences. As we move closer to 2026 and beyond, the continued evolution of digital banking promises a more efficient, inclusive, and user-centric financial landscape, fundamentally reshaping how we manage and interact with our money.